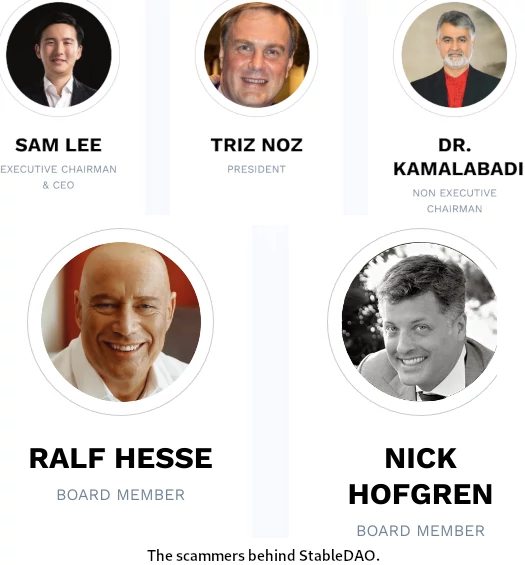

Inside Sam Lee’s Blockchain Global & ACX scams

![]() As Sam Lee gears up to defraud consumers with his new StableDAO Ponzi, proceedings in Australia are providing insight into his earliest crypto scams.

As Sam Lee gears up to defraud consumers with his new StableDAO Ponzi, proceedings in Australia are providing insight into his earliest crypto scams.

I want to preface that Blockchain Global was a cloud mining platform. Its business model is thus of course different to StableDAO and Lee’s various Hyper* Ponzi schemes.

What’s relevant with Blockchain Global is what was going on behind the scenes.

What we already know is Blockchain Global was founded by co-conspirators Lee (aka Samuel Lee, Xue Lee) and Ryan Xu (aka Zijing Xu).

What we already know is Blockchain Global was founded by co-conspirators Lee (aka Samuel Lee, Xue Lee) and Ryan Xu (aka Zijing Xu).

Blockchain Global was a cryptocurrency exchange and mining firm, starting out as Bitcoin Group.

In 2016 Bitcoin Group rebranded as Blockchain Global. In 2017 Blockchain Global spun off ACX, a cryptocurrency exchange.

Blockchain Global and ACX collapsed in 2020. Later that same year Xu and Lee fled to Dubai.

Claims received by liquidators would peg Blockchain Global and ACX losses at $48.9 million.

As liquidators and presumably also law enforcement hunted them down, Xu and Lee turning up in Dubai is no coincidence. The crime-riddled emirate is notorious for sheltering scammers from authorities.

The liquidation of Blockchain Global and ACX hit the Victorian Supreme Court earlier this week. And with that we’ve gained additional information into how Lee runs his scams.

Poor record keeping, comingling of invested funds, misappropriating investor funds for personal benefit and, ultimately, gambling away invested funds.

Sarah Danckert from the Sydney Morning Herald has been covering proceedings;

The court heard on Wednesday that Blockchain Global’s ACX exchange took the cash invested by its customer to trade cryptocurrency and mingled the funds into one pooled fund – a practice that is in breach of client money reporting rules for licensed stockbrokers and trading groups but not for the largely unregulated cryptocurrency market.

Under examination by counsel for the liquidators Andrew Silver on Wednesday, Blockchain Global’s chief technology officer, Jin Chen, said the company kept limited records of each customer’s trades and their holdings.

Invested funds were commingled with Blockchain Global’s founder’s personal funds, a loan taken out against ACX’s client balances (unknown to clients) and purported trading profits.

Chen also told the court that he was instructed by Blockchain’s co-founder Allan Guo, who held the roles of chief operating officer and chief investment officer at the group at various times, to transfer bitcoin from the pool of customer funds to other parts of the business.

Other uses of client funds included:

- investing into a cannabis themed shitcoin;

- investing in shares of a Canadian company;

- topping up Blockchain Global’s founder’s and staff’s bank accounts; and

- paying off Blockchain Global’s founder’s and staff’s mortgages

Again, none of this was disclosed to Blockchain Global and ACX clients.

Blockchain Global had told its customers their money would be held in trust while they traded on Blockchain’s popular ACX exchange.

To avoid regulatory detection, Lee and Xu set up bank accounts in staff family member’s names – none of whom had anything to do with the business.

The court heard that Blockchain Global, despite being a successful exchange with thousands of customers, kept being “debanked” by various banks, a process where a bank stops dealing with a customer because it was working in the cryptocurrency industry.

Blockchain Global used companies set up in the names of Guo’s mother and then mother-in-law to set up bank accounts from the group to make its banking process easier.

Guo also told the court Blockchain Global established another subsidiary in the name of Guo’s then wife to obtain an Austrac registration.

Allan Guo, aka Liang Guo, was Blockchain Global’s COO and CIO. He and CTO Jin Chen have been left holding the bag in Australia.

The investigation into Blockchain Global is ongoing, however Supreme Court proceedings strongly suggests $48.9 million in losses is extremely conservative.

Under examination by counsel for liquidators Andrew Silver, former company chief investment officer Allan Guo confirmed the transfers out of the company of customer funds was significant.

Probing Guo, Silver asked: “If I told you hundreds of millions of dollars had been withdrawn in this way from gateway accounts and then invested into other exchanges, what would you say to that? Would it have been hundreds of millions of dollars?”

Guo responded: “Total, yes.”

You’d be naive to think this isn’t exactly how Xu’s and Lee’s HyperCash, HyperCapital, HyperFund and Hyperverse Ponzi schemes were run.

And, more to the point given recent developments, how Lee will run StableDAO.

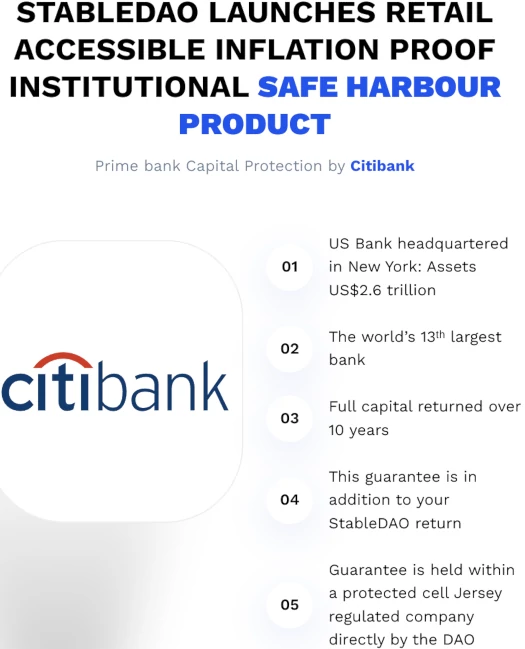

One of StableDAO’s primary marketing points is “prime bank capital protection by Citibank”.

Such to the extent StableDAO has any interaction with CitiBank, if any, I can guarantee you “StableDAO” or Sam Lee aren’t disclosed.

Given Lee and Xu haven’t been arrested yet (Xu hasn’t been seen in public since late 2021), pegging down total victim losses since HyperCash is impossible.

I can make an educated guess based on how big HyperFund got though, that consumer losses probably sit well over a billion. And most of that is believed to be from US resident investors.

And now Lee is looking to do it all over again with StableDAO.

You invest in STBL tokens, Lee and his co-conspirators, early investors and top recruiters steal your money.

Given Australian authorities have no more sway with Dubai’s corrupt officials than US authorities, I’m not sure what will come of the Blockchain Global proceedings.

We’ll keep you posted on any significant updates.

I want total info on this scamster I too deposited in his organization hypervers.

Put him behind bar if he not given our investment back.

Scam Lee …

Sam Lee and Ryan Xu need to be put behind bars ASAP. There was one very kind woman named Lisa Golda who invested her life savings into Hyperverse who died this past week of Stage 4 Cancer and she had two little children.

Because of Hyperverse she was unable to take care of her children and pay for her treatments to live longer and she begged for them to return her money for her life and they just ignored her. Very sad.

RIP Lisa Golda you will be missed.

There is a guy named Danny De Hek, he is working hard to get as much information about their whereabouts to report to the authorities to have them arrested asap!

Sam Lee new project is Vidilook, current status is they are withholding money from peoples accounts, claiming errors in the system etc initially signing up people with big returns and then overnight slashing earnings so impossible to earn your invested money back.

I am trying to warn people but they are believing the lies as the early investors have cashed in big… so sad people have invested money they really cant afford in a desperate attempt to make some money.

Covered here: https://behindmlm.com/companies/hyperfund/vidilook-slashes-daily-roi-vdl-coins-confiscated/

Anyone looking for this serial scammer he is currently in Dubai living off the funds he stole from people that invested in his latest scam called Vidilook AND trying to raise new funds on We are Satoshi meanwhile.

This guy has no shame and thinks he is invincible, he is constantly under influence and does not make any sense when he speaks.

Everyone who got scammed by him needs to send evidence to the Dubai Police as this fraudster must be stopped before he does any more damage.

I invested in Hyperverse. I was promised to earn a small income from that investment to subsadise rising expenses.

This money was part of my retirement that has been stolen from me.

Please help us in South Africa we lost millions of rands through hyperverse hypernation vidilook now stabledao. please help us get our monies and arrest this man.

People believe his tricks they deposit money unaware of being scammed. Please help stop him. Damage is huge in South Africa help.

It’s happening again.