Lyoness corporate webinar spells out Ponzi scheme

![]()

When I sat down to initially review Lyoness (the European version), I spent a few days trying to get my head around material that was obviously never written to be fully comprehended by your average MLM affiliate.

When Lyoness launched in the US, they sought to remedy this by releasing slightly less confusing business model material. Not as clear-cut as it could have been, but enough for me to suss it out and put out a Lyoness review.

In my review I identified the primary revenue source that had contributed to the initial success of Lyoness in Europe and their subsequent worldwide expansion.

That source?

An affiliate-funded investment scheme, where affiliates invest in “accounting units” and after a fixed number of new units have been invested in, Lyoness pay out affiliates a cash ROI.

All monies are deposited with and paid out by Lyoness, isolating the scheme from the merchant shopping network.

That of course doesn’t stop the company burying the scheme in mountains of “earn cashback by shopping” literature, which the companies affiliates are all too happy to run around the internet promoting.

With now over 1000+ comments on the BehindMLM review fleshing out the AU investment scheme (including the reluctant admission that it functions as a Ponzi scheme by some Lyoness affiliates), some affiliates still don’t see it, or probably more accurately, refuse to see it.

Despite the review citing the official Lyoness US compensation plan material itself, evidently there’s still a great deal of confusion amongst Lyoness affiliates as to what the business is actually about.

Evidently I’m not the only one to observe this, with Lyoness feeling the need to put together an official corporate webinar to lay out the compensation plan and business model in detail.

So here it is, straight from the horse’s mouth: The Lyoness Accounting Unit Investment Scheme.

Coming in at a gruelling 78 minutes (thankfully broken into four parts), the official corporate presentation is hosted by Rik Wahlrab (right), who credits himself as being a “Presidents Team Member” of Lyoness USA.

The first two parts of the presentation walk the viewer through the cashback scheme and generating units through this scheme. It’s not until the third part of the presentation that we get to the “meat” of the business.

Part 3 of the presentation opens with Wahlrab stating that

now we’re going to get into it, how to make money and what it’s all about.

Probably something most viewers will miss, Wahlrab is essentially admitting he just wasted the past thirty-four minutes of your life on the shopping network side of things.

Part 3 of the presentation gets stuck into becoming a Lyoness “Premium Member” and the commissions paid out to them. Wahlrab openly admits that ‘Premium Members make the most money‘, so obviously this is going to be the focal point of the presentation for prospective Lyoness affiliates.

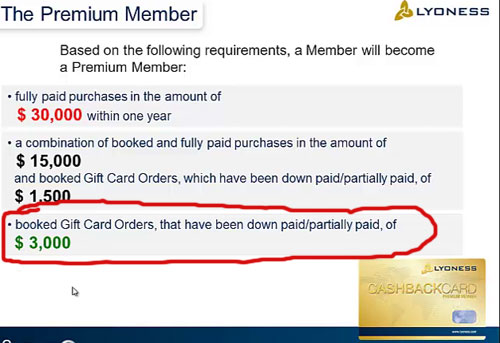

So what is a Lyoness Premium Member?

A Lyoness Premium Member is someone who has either

- spent $30,000 within the Lyoness shopping network in a year

- spent $15,000 within the Lyoness shopping network and invested $1,500 directly with Lyoness or

- invested $3000 directly with Lyoness

Wahlrab states that option 3 is ‘really what we do‘ in order to become a Lyoness Premium Member, and financially is the cheapest way for a prospective affiliate to enter the accounting unit investment scheme.

Lyoness will let you send them up to three thousand dollars and you can get units in the system now.

Why would affiliates do that?

Two reasons both of which require a fixed number (75) of new investments to be made with Lyoness by affiliates, after the initial $3000 is one is made.

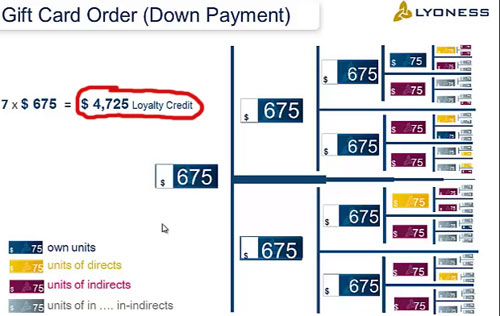

Once this condition is met, the first reason is that Lyoness pays out an affiliate $4,725 in “loyalty credit”.

In the above slide from the presentation, the blue squares represent units invested in directly by a Lyoness affiliate. The initial $3000 investment is broken down into six $75 accounting units, with each paying out an individual return once new investments have resulted in the creation of a fixed number of new accounting units after it.

This credit can then be spent with Lyoness merchants, or it can be re-invested back into Lyoness to generate more accounting units (taken from the Lyoness “Cashback Summary” document, page 2):

The Loyalty Credit can be paid as Cash or use as Accounting Units to grow additional income.

The second reason, and this is as blatant a Ponzi scheme as you can get, is that Lyoness will also pay you straight cash on top of the loyalty credit.

Referred to as “loyalty commission”, on a single $3000 Premium Member investment (6 x $75) Lyoness will pay you a $1386 cash ROI, once 70 new investments have been made after yours:

For those of you who are mathematically inclined, you’ve probably worked out that seven times $75 is only $525. Before we get into where the rest of the $3000 went, it’s important to drill home the point that an affiliate deposits $525 directly with Lyoness, and is paid $1386 in cash once a fixed number of new $75 investments have been made.

This equates to a 264% ROI. On top of this they also give you $4725 in credit, which can be re-invested back into the scheme to generate more accounting units.

And how do I qualify to earn my cash ROI?

Simple – I have to recruit at least one new investor Lyoness affiliate who then also makes at least one $75 investment into the scheme:

Now, despite the answer being rather obvious, the question arises: “So where does this money come from?”

Lyoness would have you believe, as Wahlrab repeatedly claims throughout the presentation, that it comes from Lyoness’ participating shopping network merchants. The problem with this claim though is that it doesn’t add up.

As a Lyoness Premium Member (or regular affiliate who decides to invest in accounting units, after “buying” $300 in giftcards), I deposit money with Lyoness, recruit one new investor who invests in at least one $75 unit, wait till enough new investments have been made (70 in total), and get paid my cash and loyalty credit ROI.

If I re-invest my loyalty credit back into AUs, I bypass shopping merchants altogether.

All money is deposited by affiliates with Lyoness and all money is paid out to affiliates by Lyoness.

Logically, that means the money Lyoness is paying affiliates is being sourced from… wait for it, none other than affiliates.

You invest $75, once Lyoness has collected $5250 (70 * $75), they pay you and the scheme continues along as new money continues to be pumped into the scheme by affiliates.

Technically it can keep going on shopping generated units but, and let’s not kid ourselves, this is just a front for the investment scheme. The revenue generated by shopping, as per analysis of the Lyoness Income Disclosure Statement, is entirely negligible.

Wahlrab even go so far as to refer to gloss over the process with which units created via shopping as “yada, yada, yada” at one point in the presentation.

Now, getting back to the remaining $2475 Lyoness Premium Members invest? Well here’s where things get even more murky.

The $75 accounting unit investment scheme is only the tip of the iceberg, with Lyoness operating an additional four levels of accounting unit investment above it.

There are five in total (including the $75 level), offering ROIs on investments ranging between $75 up to $24,000:

The gold box in the above screenshot shows you where the rest of the $2475 of Lyoness Premium Member investments go, that being into what they call the ACII ($225) and ACIII ($600) investment schemes.

Oh and note the red circles I’ve added, they are the cash ROIs paid out at each level, once an affiliates investment reaches maturity (subject to a fixed number of new investments being made).

Note that Lyoness don’t initially allow affiliate to directly invest in the upper two AC levels:

They don’t let us make downpayments into those last two accounting programs, at least in the beginning.

Why?

Because then Lyoness would only be for rich people, right?

For $3000, Lyoness Premium Members get seven $75 units, three $225 units and three $600 units:

Rik Wahlrab strongly urges viewers of the Lyoness corporate presentation to get in at the $3000 Premium Members level, but for those who don’t have $3000 he still urges them “get started at whatever amount you can”.

A $1050 amount is recommended, allowing a Lyoness affiliate to invest in three $75 units and one $225 and $600 unit.

If you do that at least you’ve got units here and here (ACII and ACIII), and you’re not fully missing out.

I would recommend that if you can’t do three thousand, at least do a thousand fifty… or something beyond that so you’ve got units in ACII and ACIII.

What do you get paid back for your $1350 (four additional $75 units over $1050)?

$12,360. That’s awesome.

Supposedly justifying the blatant affiliate-funded Ponzi scheme Lyoness are running above is the requirement to purchase $600 in giftcards with every $3000 investment downpayment.

How that negates Lyoness’ accounting unit investment scheme from being an unregistered security I have no idea, but that’s the premise they sell to prospective affiliates.

Just to ram the point home, you invest $3000 as a Lyoness Premium Member, spend $600 on giftcards, and Lyoness pay you a $9108 (303%) ROI once seventy $75 investments, 60 $225 investments and fifty $600 investments have been made after each of your units respectively.

So $600 worth of giftcards will allow you to make a $3000 downpayment, now you’re fully covered and look what you get back – twenty four thousand eight hundred and fifty eight dollars for your one-time three thousand dollars.

Finally, whacked on top of all this is a progressive cash ROI paid out incrementally as new investments are made:

As per the above table, one single $75 accounting unit can progress (paying out the affiliate who invested in it), incrementally all the way from ACI to ACV.

You can imagine that you’ve got units that are gunna move through the system. Maybe it takes a few years to move all the way through, you know, depending on how many people are connected to you but so what, right?

This is what it eventually pays out. It just keeps going and going and going, based on other people simply

shopping andcreating units.

Rik Wahlrab states in the Presentation that ‘he was the first “level 7” in North America’. What does that entail? At least 20,000 “career points” being generated via the creation of accounting units following Wahlrab joining Lyoness.

For his efforts, as a Level 7 Lyoness affiliate Wahlrab takes home an additional $30,000 a month on top of any ROIs paid out as a result of his participation in the accounting unit investment scheme.

Sign up as a Lyoness affiliate, invest your $3000, wait for 20,000 career points to be generated via the creation of accounting units after your own (you can help create them by re-investing), and you too can reach the level of success Wahlrab has achieved within the Lyoness investment scheme.

Wahrab goes on to predict that

there are going to be thousands of people making Presidents Team, Level 7 and Level 8, in the United States. Thousands, many thousands.

Who’s it going to be?

It’s going to be those that get started now isn’t it. It’s those of us who get started now and start sharing Lyoness.

The people who get started now, the people who get started early when it’s very small – they’re kind of pioneers. But on the other hand, they’re going to benefit for ever and ever and ever and ever.

…and if you don’t do it, someone else will.

Good grief.

Footnote: Credit to the “Complaint Center Lyoness” blog for making public footage of the Rik Wahlrab’s Lyoness corporate webinar.

I’ve included the footage from the relevant parts quoted in this article (parts 3 and 4) below:

This explains Jeanette Hayworth’s comment #401 in the long thread, where she claimed Dr. Wahlrab had explained the system for her back in July 2012.

I asked her why she used a chiropractor as investment advisor, since most experienced people know that dentists are much more qualified as investment advisors. She never returned, but posted a comment on her own blog. She obviously doesn’t like jokes about her investment ideas.

@Oz

If the unit comes from yourself and your direct downline, plus a few spillovers from direct upline, that normally translates to “pyramid scheme” (not to “Ponzi”).

Pyramid schemses have money being paid in under your own, e.g. “positions” under your own position, until you have filled your personal matrix with enough positions to generate a payout (“cycle”).

Ponzi schemes don’t have “positions”, but they CAN have. The primary “everyone can earn money” generator is an imaginary “money generator”, e.g. a penny auction, autosurf, paytoclick, fake work, virtual investments, and so on, where you don’t need to recruit people to earn a positive ROI.

Lyoness CAN be a Ponzi scheme (the system itself), but it CLEARLY is a pyramid scheme in the way payouts are being generated to the members. There’s no “money generator” other than the recruitment based one.

Lyoness clearly have money coming in into “positions” directly under your own positions. Each of your own unit positions can have 2 unit positions directly underneath (sideways for Lyoness).

THE MATRIX SYSTEM FOR AC1 – AC5

Down payment matrix, the matrix model itself:

Above: 1-2-4-8-16-32- etc.

Unit 1 ————————-

Below: 1-2-4-8-16-32- etc.

AC1 matrix filled:

Above: 1-2-4-8-16-4 = 35 sub units

Unit 1 ————————-

Below: 1-2-4-8-16-4 = 35 sub units

AC2 matrix filled:

Above: 1-2-4-8-15 = 30 sub units

Unit 1 ————————-

Below: 1-2-4-8-15 = 30 sub units

AC3, AC4, AC5 matrices filled:

Above: 1-2-4-8-10 = 25 sub units

Unit 1 ————————-

Below: 1-2-4-8-10 = 25 sub units

Your personal down payment plan is “Unit 1” (in the middle). It’s a “position unit” rather than a “sub unit”, i.e. it can generate “maturity payouts” for the member when a matrix is filled.

“Sub units” can come from yourself or from other members, from down payments or from “Loyalty Benefits” (paid by merchants).

* Your personal matrix is probably flushed when a down payment order is “filled”, flushing 35 above / 35 below (in AC1), keeping unit 1, refilling the positions in the “strong leg” with sub units from deeper down in your lifeline, e.g. if you have 50 sub units above and 35 below the 15 leftovers above will enter new positions in your “personal down payment plan”.

* “Flushing” means the sub units are removed from your personal down payment plan, but not from the system itself. The sub units will still exist in other members plans, and in a main matrix.

FILLING A MATRIX

Your “unit 1” is a “position unit” in your personal plan, paid for by qualifying as a member. It’s the membership itself, booked into the first down payment agreement AC1. It can also be booked or rebooked into higher AC’s.

The first units above or below can come from yourself or from someone directly recruited by you, from down payments or from purchases (Loyalty Benefits from merchants).

* They can also be generated by upline members in direct upline (1 sponsor, 1 sponsor’s sponsor, and so on).

* They can also be generated as bonus units with reduced cash payouts.

* But normally you’ll need to initiate the very first units yourself, above and below. “Initiate” = it can be done indirectly.

Actually, chiropractors makes the best woo salesman, because chiropractic itself is pseudoscience, and thus its practitioners are well-versed in talking bull****. It takes little training to make them apply the same ability to bull**** to pseudo-economics (i.e. scamming)

He generates 20,000 Career Points (not units) per month (or he has DONE that in the last 6 months).

1 AU in AC1 = 1 Career Point (AU cost = $75)

1 AU in AC2 = 3 Career Points (AU cost = 3*$75)

1 AU in AC3 = 8 Career Points (AU cost = 8*$75)

1 AU in AC4 = 24 Career Points (AU cost = 24*$75)

1 AU in AC5 = 80 Career Points (AU cost = 80*$75)

The plan “invest one $75 unit, and just wait for other units to be generated under you” won’t work. It will only generate random units from your upline, and most units generated that way will bypass your position.

To make it work, you will need to recruit recruiters in both “legs”. Lyoness doesn’t have any other systems generating units for you than your own recruitment, and your directs’ and indirects’ recruitment.

It doesn’t have any “magic unit generator” other than a “bonus unit generator” and a “unit rebooking system”, and both will require recruitment from you / your downline to work.

Where in that presentations is about “investment” ?. Its only downpayements. Downpayments is legal or is not legal?

If a 1000 person make a downpayments for vaccantion is a Ponzi? Regular company if receive that downpayments is in a Ponzi? What happens with that downpayments if person changes his mind?

Dentists have all the connections, directly and indirectly, e.g. to gold-suppliers.

Actually, the dentist comment was meant as a joke. She presented her statements in a way that led me to believe Dr. Wahlrab’s profession and title was important, e.g. “I have asked Dr. Wahlrab about it, the most famous financial advisor in the US”.

So I googled him, and found that he was a chiropractor. She didn’t mention anything about positions in Lyoness, only that he was Dr. Wahlrab.

@nelson

Downpayments don’t generate cash ROIs, investments do.

And don’t waste our time trying to compare Lyoness’s investments with non MLM ROI paying downpayments in other industries.

I suppose technically I’d classify Lyoness as a Ponzi/pyramid hybrid. The ROIs are generated via investment in units, however an affilaite does need to recruit a minimum of four new investors to get their ROI.

Once that’s done theoretically an affiliate could fund their own ROIs (by investing in a crapload of AUs), however that’s clearly not logical for obvious reasons.

The re-investment mechanic and positions correlating to specific monetary values over your typical new affiliate = one position in the comp plan differs from your standard pyramid scheme. Lyoness is somewhere in the middle (think Speak Asia).

Oops thanks for the pickup. I did have to fight off the sleepies towards the end of the presentation there (yeah, I watched the whole thing).

I mistook points for being generated with each AU, not realising he was only talking 1:1 at the ACI level. I’ve fixed the review to reflect this.

It is specify in law that? If the integral payments generate ROI then I think downpayments must generate ROI.

Yeah… the law of common sense.

You can use whatever terms you want – an investment generates a ROI, downpayments do not.

Your conclusion about “Ponzi” is probably correct enough. Lyoness HAS elements similar to a Ponzi scheme. But arguments used in the logics are slightly flawed, and it won’t work in reality either.

“Ponzi/pyramid hybrid” is correct enough, since it will cover typical characteristics for both.

LOGICAL RULES

One of the logical rules is the “bigger group, smaller group” rule:

* A smaller group can be part of a bigger group.

* A bigger group can not be part of a smaller group.

Another rule is the rule about different groups, not part of each other directly, but sharing some common similarities, and often (but not automatically) parts of the same bigger group higher up in the system.

Example:

* All men have hair in their faces

* Aristoteles has hair in his face

* Aristoteles is a man (flawed logic)

Aristoteles is actually a monkey. He belongs in the same bigger groups “primates” and “mammals” as all men do, but he doesn’t belong in the same smaller group “homo sapiens”.

The fact that someone named the monkey “Aristoteles” doesn’t make him a man or a human. The fact that he has hair in his face doesn’t make him a man either. It was easier to identify his true place in the system when I identified the bigger groups “mammals” and “primates”

Ponzies and pyramids probably belong in different small groups, and they probably belong in the same bigger group higher up in the system.

Ponzi schemes CAN belong in the group INVESTMENT FRAUDS, but the term “investment” isn’t typical enough to define it.

TECHNICAL DEFINITIONS

I’m not professional, so these definitions will probably need some corrections.

A Ponzi scheme is technically

* a plan or a system

* where participants gives consideration

* for a prospected potential to earn financial gains

* that are prospected to derive from profitable activities

* but where the prospected profitable activities are falsified, misleading, non-existent or otherwise fraudulent

* where any financial gains primarily derives from other participants rather than from the prospected profitable activities

A promotional pyramid is technically

* a plan or a system

* where participants gives considerations

* for a prospected right to earn financial gains

* that primarily derives from other participants being introduced into the plan

* rather than from sales or consumption of goods or services

It’s difficult to understand the logics you’re using, other than that you’re probably trying to justify the use of down payments as some type of “commonly used business practice, perfectly legal since it’s not forbidden by any law, and is used by other businesses as a common practice”.

I can follow that logic, but not the ROI idea.

“Commonly used business practice”?

Actually, it isn’t. Down payments are used for special purposes in business, and are not common in normal trade.

“Perfectly legal / not forbidden”?

It isn’t illegal in itself, and isn’t regulated directly by any specific law. The practice isn’t protected by any laws either.

It’s regulated by different “Common Sense Rules”. Laws will not regulate each and every aspects in a society, people will need to use their own brains most of the time.

“Used by other businesses”?

That doesn’t define whether something is legal/illegal. With that logic, everyone can do anything if they can find some others doing something similar. It doesn’t need to be very similar either, the most important parts were about “not forbidden by law AND used by others”.

What exactly does your gut feeling tell you about Lyoness and the down payments? Does it tell you that the system is perfectly legal, and that anyone believing otherwise must have been heavily misguided by their own negativity?

Can no disagree with you more. I used chiropractor for three separated conditions, and he fixed two of them. It was way better than invasive surgery

Yes, there are specific laws about that. Ask the SEC.

Only companies that issued registered securities (stocks, bonds, hedge find units and so on) can offer ROI. There are some exclusions for private investment clubs, but they also strictly governed to who they can sell, how much they can advertise, maximum investment amounts).

None of these companies is allowed to do MLM type recruiting.

You are saying that it is specified in the law that if integral payments generate an ROI then a down payment must also generate an ROI?

It would seem so since they are both part of a common investment, but there could also be some provision in the contract to the contrary.

The express terms of a contract will generally govern the parties providing other factors are equal. Its useful knowing the statutes but you really need to understand what the contract says too.

When terminology such as “integral payments” are not commonly understood, in common useage, or are subject to interpretation a well crafted contract will define the terminology used.

I avoided the use of “investment” for the Ponzi scheme definition, to be able to test it against other definitions

* a plan or a system

* where participants gives consideration (typically about paying money to the organizers, but not limited to that)

* for prospected financial gains

* both are some type of FRAUD, primarily about money

* Pyramid schemes are recruitment driven, “recruit a huge downline to maximize your profit”.

* The fraudulent part is within the business model itself, a non-sustainable business model. It will run out of new participants and collapse / slow down.

* Ponzi schemes are driven by false promises, “invest more and you will earn more” or “pay for more AdCentrals, and you will receive a higher weekly salary”.

* The fraudulent parts are within how these schemes presents their own business ideas to potential and existing participants;

* in how they distribute false profit / false promises about profit;

* in how they use money from the participants themselves (as a group) to support payouts.

“False promises” is a more significant identifier for Ponzi schemes than “investment”. It’s typically about anything people can be willing to believe is profitable enough to generate a profit or ROI, making them willing to spend or invest money.

* The false/misleading promise has to be FRAUDULENTLY presented, in an attempt to mislead people to spend or invest money in a way they wouldn’t have done if they had been given honest and correct information.

Lyoness qualifies as a Ponzi scheme in the false promises part (but that doesn’t alone qualify it as a Ponzi).

“People will always shop” is one of the main arguments used to defend the sustainability of the program, i.e. that the bottom levels of the pyramid structure will be filled with ordinary shoppers generating payouts for the lower levels of paying participants.

Lyoness is clearly misleading people in several different ways. The system is almost impossible to understand properly, and most claims are misleading and/or falsified.

Just my two cents. If “People will always shop” lead to profitability than most retail stores were wildly profitable. And we all know it is not the case.

I also expect at some time insinuation about mysterious “external sources of revenue”. A lost of ponzies make this insinuation when they get in trouble.

Perhaps what they REALLY meant is “there’s a sucker born every minute” (usually misattributed to P.T. Barnum)

It’s illegal to pay commissions on down payments or lay away / lay-buys. Just look what happened to Gold Quest with their deposit on a gold coin plan. USA smacked them Australia banned them and so did many other countries which forced GQI to change their entire marketing plan.

GQI made 100’s of million initially, then they got pulled up but by then they had a made a fortune. If they tried to do a start up now with the plan and products minus Gold Coins, they have currently they would not experience them same stella success they had initially.

After reading this excellent report i see that Lyiness is running a lay buy system with a 2 x 4 splitting matrix. Really old school stuff and definitely something the authorities i would have thought would have been all over sooner.

Its a Ponzi in Drag.

But what proof do you have other than “it seems to have helped”? Correlation is not causation without further evidence.

I understand many people BELIEVE it helped, but what you have is merely correlation. You have no proof it was causation, much less prove that it worked “better” than traditional treatment… or no treatment at all.

On the other hand, there’s plenty of scientific studies that chiropractics is pseudo-science. AMA’s official position on chiropractics has not changed: quackery. It merely no longer publicly oppose them.

http://www.skepdic.com/chiro.html

As this is NOT a debate on chiropractics, I’ll stop here. I accept plenty of people BELIEVE chiropractics worked for them. However, there’s no scientific evidence proving so, and thus, that makes it pseudo-science.

I had a curvature of the spine. Do not now exact technical term. Spine looked like a wave. Problems with the neck. I had difficulty freely moving neck. Also, pain in the spine area due to pinched nerve.

All of that was fixed. Normal spine. No stiffness in the neck. No pain in the back. Nerve was not pinched anymore.

You maybe were thinking about acupuncture. That was a waste of time and money.

Acupuncture is a different type of woo it believes in redirecting the flow of “qi” (pronounced chee) through use of needles at nerve points.

In that sense, it’s not that different from chiropractics, where it believes that through manipulating the spine it can fix “subluxation”, or the misalignment of nerve signals passed along the spine.

Sill can not agree with you. Chiropractics is good for quite few good things(release pinched nerve, realign spine in younger patients, fix neck problems), and I am testament to that. But if Chiropractor says that he can eliminate deceases or make you feel younger just by realigning the spine, he is full of crap.

Acupuncture is a 100% bogus. I read few studies and there is no difference of “work” between “master” acupuncturist, newbie who only knows how do no harm and placebo.

Shouldn’t that be “massage therapists” or such?

The fact remains that chiropractic medicine was founded in 1895 by a magnet healer (i.e. bogus). And subluxation is bogus. I’m sure it helped, but it’s probably the massage and relaxation that helped, not the principle of chiropratics.

Troy Dooly’s new video on Lyoness. http://www.youtube.com/watch?v=cAvTNUGCK2M#at=305

@NHRA… Troy is truly a moron, he states Lyoness is from Australia, twice. When it’s Austria. Talk about basic fact checking 🙂

It’s pretty obvious he was talking to Mr. Clements. IMHO, of course. 😉

Len Clements (Troy Dooly) had some new information we didn’t know about, e.g. about additional investments in other markets.

He also had some confusing logics, e.g. when he insisted on calling the units for “profit centers”. I believe some of his mathematical conclusions are wrong, but other conclusions seems to be correct.

His primary conclusion was pyramid scheme, based on how the payouts are organized rather than on how investments are made. That part of the logic actually makes a lot of sense, in that he organized the different parts into identifiable structures “binary”, “unilevel”, “cycle” etc.

His secondary conclusion was Ponzi scheme, based on the prospected returns and how investments are made. But I believe his mathematical logic has some flaws, e.g. I could have accepted it if he had called the first unit for “profit center”, but defining all of them as “profit centers” doesn’t make much sense.

Link:

http://mlmhelpdesk.com/lyoness-america-violating-pyramid-ponzi-business-opportunty-security-regulations/

“The biggest red flag in Lyoness is all the confusion”. He added some valuable logic to it and some new information, but he also added his own confusion.

Mr. Clements had said he was “investigating” Lyoness for a long time, many months ago. I think he had a few comments here soliciting information.

I’m glad he finally got the conclusion out. His investigation of Zeek was published AFTER Zeek got shut down. 🙂 I think he’s intimately familiar with pyramid schemes, but not so much with Ponzi schemes.

Ponzi is paying members with “new” members money. Whats a pyramid scheme then ? Aren’t they pretty much the same? 🙂

Pyramid scheme involves recruiting new members, and is dependent on recruiting, and have incentives for doing so, like “complete a matrix” or specific recruitment bonuses (recruit X, get Y).

Ponzi usually doesn’t have recruiting requirements or incentives to recruit.

The two are cousins, but pyramid schemes are a bit easier to find as the recruitment requirement/incentive is quite obvious. Ponzis are a bit harder to identify as you need to confirm the lack of other sources of income.

http://amlmskeptic.blogspot.com/2012/06/mlm-basic-what-is-ponzi-scheme-and-what.html

That’s the typical disadvantage in becoming “expert” on something = you feel you have to deliver MORE than others. But the market would probably have accepted a lower standard.

I actually “sold” his report in the other Lyoness thread. “Selling” something = “make people accept something as it is / make them feel it has some special value”. Or other ideas similar to that.

Here’s the result:

I actually made most of it up, but it was based on logical analysis rather than pure fantasy.

That’s the other disadvantage in becoming an “expert”. People can’t easily point out logical flaws without potentially coming in conflict with that role.

My ONLY intention for linking to that report was because it contained organized info I believed the other reader(s) could be interested in.

I spoke to a Dallas business intimately involved with Lyoness. He says Lyoness does indeed generate an income stream through the discounts they negotiate with businesses – varying between 1-20% depending on the business.

Thus they stay in positive cash flow despite payouts of bonuses and commissions by being merchant driven. Were you even aware of this?

If not, why?

Also, in the film sighted above, Dr. Wahlrab states that one should NOT purchase the partial gift card premium plan unless he wants to do the business end of it. Otherwise one is encouraged to just to shop and enjoy the cashback benefits.

I have been told that only 10,000 people of the initial 80,000 US members have prepaid for the units, leaving the vast majority as simply shoppers.

And the sinister reason for the AU purchase is primarily for those involved in the business end to position themselves at the head of their business so as to capture the other AU created behind them, since it is possible for one of their recruits to pass them, and thus lose credit for the AU.

Remember, accounting units are created from the discounts provided by the merchants – they are real money.

Premium members pay $3000 for 13 accounting units spread over 3 levels, which are considered partially paid gift cards, and then $600 for gift cards. The $3,000 can be redeemed any time through shopping with them until they are fully recovered.

The $600 in gift cards can be spent on any merchant offering gift cards. Thus the investment can be fully recovered. And for gosh sakes, all this fuss over a potential $1500-3000 upfront payment, which represents your maximum risk. I have lost that much in 10 minutes in the stock market!

In summary:

All members are being encouraged to join as shoppers and only join as premiums if they want to pursue the business end.

Lyoness funds its program primarily through an income stream generated by merchant discounts paid to them in order to bring in loyal new shoppers who will come back time and time again, without having to pay for any advertising and leading to increased revenues for the merchant.

I have been told that Lyoness will likely drop the opportunity to even come in as a premium member by next year, thus doing away with the partially paid gift card concept.

The so called pyramid you describe is made up of accounting units, not people, generated by shopping and sharing, since no further units can be purchased after the initial individual $3000 investment, unless another member wants to see you his.

Yes, you can invest in other countries, but most members will not. And members have the opportunity to pass other members and move up the chain.

Finally, their shopping network is really fun to do. You do get cashback on every purchase, and get great deals with online shopping. And you are paid cashback every week, right into your checking account. The Loyalty benefits do accrue and do get paid out through shopping and sharing.

Why didn’t you just look at Lyoness’ business model and compensation plan?

Here we go again…

The shopping merchant network is fine in and of itself but it doesn’t account for the thousands of dollars paid out via the accounting unit investment scheme. All monies are paid to and by Lyoness, with that money being sourced from affiliates.

Merchants have nothing to do with the AU investment scheme. Seriously, just think about the logic here, you get a cash back on top of a cash ROI if enough AUs are invested in after your own? Merchants schmerchants, Lyoness themselves pay out the cash component of the ROI.

Well we’re discussing precisely the business end of Lyoness, that being the accounting unit investment scheme.

Told by whom? Did you see any official company documentation stating at much?

Revenue wise, even if it’s 10,000 / 80,000 split between premium members and shoppers, care to take a stab at the commissions paid out between the two groups?

You’ll find just a tiny fraction of the 10,000 investors dwarfing the money paid out to the 80,000 non-investors. Nobody who’s made any significant money in Lyoness has done so via shopping, it’s all AU investment.

Yeah, invest early so as to reap the maximum benefit from those investing after you. That’s your typical Ponzi scheme investment strategy.

Considered by whom? Revenue wise affiliate pay Lyoness $3000, who then pay them back >$3000 after enough new $3000 payments have been made by other affiliates. This has absolutely nothing to do with the merchant shopping network.

And this is what happens when you “talk to someone” instead of just going straight to the Lyoness compensation plan. Simply put, it’s a load of bullshit. Affiliates can invest into Lyoness as much as their own funds permit. There are no restrictions.

And even if they were implemented, it still doesn’t change the core mechanic of an affiliate’s ROI being paid out subject to a fixed number of new investments in AUs being made.

Pure Ponzi.

Affiliates join Lyoness, invest $x directly with the company and receive a >$x ROI after enough new investments have been made by newly recruited or existing affiliates.

It’s a Ponzi scheme, irrespective of the attached shopping merchant network. End of story.

Next time you talk to “the Dallas business”, ask them how many thousands of dollars they’ve invested in Lyoness AUs and how many they’d like you to invest if you joined under them.

@Oz, it’s unforutnate my mother get involved into this because an upline from her previous company talked this up like being the next best thing since sliced bread. *sigh*

You probably didn’t listen correctly. The DISCOUNTS vary between 1-20%, but the actual revenue paid to Lyoness is 0.5%. Says so in the business enrollment kit. That, and a tiny annual fee plus some expensive Lyoness brochures.

If the business choose to give a 2% discount, it actually is paying 4.5%… 2% to you, 2% to your upline, and 0.5% to Lyoness.

So yes, it does have income stream, but is it really enough to pay out all the AUs?

There is no “business”, esp if you “buy into it” by paying for the AU. “Making downpayment on a gift card” is not a business. The two explanations don’t even fit together! It seems whoever you asked is just making it up as he went along. So do you trust the OFFICIAL explanation, the unofficial one, or NEITHER?

“I have been told …”

It’s impossible to separate any facts from fictions in your story. You’re clearly repeating something you have been told or have made up yourself, but without verifying the statements in any other way.

It’s simply CONFUSING trying to analyse your statements for factual content. So I’ll guess you have been told that “You can use a method like this if you like to confuse people.”?

An what is the conclusion to that? “They are real money”? Thanks for bringing that up, we would probably never have thought of that ourselves, that cashbacks and member benefits from the merchants are real money. 🙂

Please ask him to give you the most important parts in writings, where the arguments and the conclusions are logically sorted rather than retold as a story?

E.G. if he want to tell the world that all the payouts in Lyoness derives from the merchants, then he can probably put up a calculation or something showing HOW that happens.

* when members are buying products …

* when members are making down payments …

Your version of it ended up being a confusing story, e.g. arguments without any conclusions, arguments that only tells a part of the story, arguments like the example I quoted in this comment.

If you have any important points at all, then PLEASE get them in writings from your friend.

I realize you trust hearsay evidence, because you said “I’ve been told” a lot, but have you actually tried to verify all you’ve been told, through your own research and checking Lyoness literature, like brochures, websites, and such?

And if you trust what other people say, why don’t you trust what we say? Perhaps you’re prejudiced against us “nay sayers” because you believe in this business? WHY do you believe in it? Is it merely faith?

Or perhaps you’ll look for some REAL EVIDENCE to support your conclusions? And be fair here… to yourself. After all, you have to make up your own mind, and it’s YOUR money at stake.

The “I’ve been told” can be reality, but it can also be a defense strategy when telling BS.

You can blame someone else if you’re caught in a lie, and you can’t be expected to answer too complicated questions about anything. That’s why I asked him to get the most important points in writings, logically organized rather than retold as a “story”.

The next time anyone is trying a strategy like that, I will probably bring in all the things I have been told, e.g. “A reliable source told me that Hubert Freidl have been observed in the dark strangling cats”. 🙂

When people repeatedly are using a method that will allow them to tell BS, I will normally guess they know what they’re doing and really need to use a method like that. Otherwise, it wouldn’t make much sense using it.

BS is about “half truths” in this case, e.g. statements where people will need to assume something to finish a conclusion.

Another point (continued from my previous post) …

David did simply not reflect being a real “I’ve been told” guy, one who really have heard something about the business from someone else.

* What type of weird business man in Dallas would focus on details like that when discussing or presenting a business?

* What type of weird customer, friend or whatever will ask about details like that?

Here’s an example:

They must have had a very detailed discussion before the business man in Dallas brought that up? It isn’t exactly something people randomly brings up in a conversation.

“I’ve been told” is simply a METHOD people can use when they don’t like to face the risk of being directly caught in telling BS, and David used it repeatedly. Being caught in using a method or being caught in a fake role doesn’t seem to bother them that much.

I first understand that nothing I will say or show will sway any of your opinions or views on Lyoness. Lets just get that out of the way first.

I appreciate David, taking a shot at showing how Lyoness is not a Scam, Pyramid, Ponzi etc. – I have been in 3 other MLM’s in the past and said I would NEVER get involved in an MLM again. That being said I am a Premium Member in Lyoness and a Merchant as well.

I consider Hubert to be somewhat of a genius for putting this whole thing together so I am showing my Bias.

If David said he talked to the Attorney General, or 50 lawyers and named them you people here would still discredit anything he says. That is a fact. SInce you can HIDE behind a blog and never meet people in person or stand in front you can be VERY comfortable in saying and berating anyone that disagrees with you.

Facts about any private company are hard to come by..most of what you people have said is true in that instance. – the company has no reason to put out their internals.

the Income Disclosure Statement that ALL MLM companies must present is there for the taking – Lyoness is not hiding anything. – here you go – http://cdnlarge.lyoness.net/downloads/pdf/us/download/infos/lyo-ids-us.pdf?be5c15176ca77b55c5c0c1e5a9cca0e2e82041cb3ba41e087f5cbcd7421c6b3503c5

Now on to the quotes.

Anyone who is not a Lyoness member and who is not shown the entire comprehensive business model is going to assimilate this to something they have already seen before. Everything you people rip on about Lyoness can be explained IF you are open to actual facts. If not then this is trivial and a waste of anyones time.

The shopping network is what is driving EVERYTHING in Lyoness. – Lyoness does not make money off the People putting money into Lyoness as an Investment. Now lets consider that the Gift Card Down Payments…which will be done away with in the near future…and ONLY shown as a viable means to Turbocharge you BUSINESS….not your shopping.

The reason the IDS shows that 86% of people who are signed up with Lyoness make and avg. of 12.59 per year is because they were signed up as SHOPPERS not business builders.

There is NO barrier to entry…no membership fee, no annual fee, no monthly fee or auto ship. – once they purchase SOMETHING within the Lyoness shopping community worldwide…they are members for LIFE.

If we JUST take that fact and focus on it…how many other MLM’s or network marketing models are based or even have a path to an income stream for free? – can you name one?

Every other MLM is garage certified and each “member” is a distributor. They ask you for MONEY UP FRONT which then pays the person or persons up the line. – sound a little like a Ponzi or Pyramid to you? – it should… that is what ALL MLMs are based on.

Lyoness is ONLY registered as an MLM in the USA – all the other 42 countries it is NOT. How many other MLM or Network Marketing companies can say that.

Now…if someone were to enroll a member with no barrier to entry and no fees or anything to stay a member…why would they leave?….they DON’T.

A year ago they had a decent online presence of around 250-300 large Key merchants ONLINE and 6 that were gift card merchants such as Walmart, Kmart, Chevron, Exxon, and Outback, BP. that is because you cant buy gas online (they actually had Vons at one time and are now bringing on two more grocery chains in the near future).

This is to show people that IF and ONLY IF they are making purchases at the same places that they can get a benefit they will not receive anywhere else. – Not their bank, not their individual reward cards or anywhere.

The opportunity to marry cash back with every purchase (not a big deal to most people but it is something? gimmick? – maybe but if i can use the card at roughly 2000 merchants today and growing exponentially then why wouldn’t I….especially if i am a coupon cutter or online deal finder.

At this point did I pay to join? – was a pressured into putting “in” any money? – Do i HAVE To shop? no. DO YOU know people who shop who MAY be interested in this?

A year ago there was barely any Brick and Mortar merchants. – now there are 1364 and growing DAILY. – a year ago they put on 5 -10 every 2 weeks. They are in my calculating from the past month putting on an average of 6 per day. That is actually exciting.

Now lets just talk for a moment about the statement that talks about

ALL payments to members come from the merchants. – Period.

If you understand the progression of the accounting units (either by shopping or downpayment or bonus) then you realize there is a CRAP load of shopping that goes on before people are paid on these. – 70 units after your booked unit and you get paid 675.00 – if you are an IBR (4 directs with at least 1 unit from either shopping or down payments) then you get another 198.00 on top of that “along the way”.

To most people in Lyoness this will take the longest time BUT how much effort was put into this since you were already buying stuff anyway AND telling others about it.

Has the process of education about shopping been perfect… ABSOLUTELY NOT…is it getting better and easier and more efficient?….ABSOLUTELY….are there more and more places to use that card coming online every day?…..YES.

And by the way once a merchant pays the merchant fee ONE time….they don’t pay a single cent unless a Lyoness member comes in and uses their services/products. NOBODY can argue the value in that….can you?

The KEY accounts (mostly online) …the large shopping places we all know and love….are JUST merchants for Lyoness members….so they ONLY benefit with MORE customers…and loyal ones at that.

The SME or small/medium sized merchant is the REAL winner here in this whole process since they get the best of BOTH worlds…they understand Lyoness and where it is going but they can now benefit from something no other program has ever offered. – The ability to make money when you clients use your competition.

The Lyoness SME program offers the ability to signup their own customers for their OWN rewards program (how much would THAT cost them to institute one of their own and ONLY for them) and benefit when they shop at the other 30,000 merchants worldwide.

I know this may seem like a rah rah session but I can only tell you I have done MY due diligence on this and it keeps getting better and better the more i hear about it.

Funny how you seem to skip over the Charity aspect of Lyoness. – it is plastered ALL over our sites and yet not mentioned here. – Are there scams out there for charities? Absolutely.

In fact I am always skeptical about how much goes to ANY charity of money i give. But I have seen the projects the Lyoness has done charity wise IN PERSON. As the company grows…so does the amount of benefit for those less fortunate….THAT in itself would be worth anyone taking a look at this…

PLUS even if it were a shake or a pill or changing peoples buying habits it would actually be worth doing if i were convinced of that….but with Lyoness you don’t have to do anything different to your buying habits…. I love that.

Merchants can be brought on by other members…I have 7 attached to me. They have EVERYTHING to do with AU process.

They get new clients they never had before…they are giving 2% -20% on average back to Lyoness at the end of the month of ONLY the people that are Lyoness members whether they signed them up or not. – Marketing dollars well spent in my opinion since most of those places do advertising and cross their fingers. – this is a gift that keeps giving.

I made my First shopping unit almost exclusively on local merchants that I brought in – double dipping actually which by the way you can do with your own amex or credit card since you get points or miles and or rewards with those as well… you gotta pay the merchant somehow right?

The ROI as you call it is untrue. – Lyoness does not pay out to members…If you do the math on the comp plan (the REAL math…not just picking certain parts of it) all money comes from the merchants.

Lyoness pays you handsomely for building a NETWORK of shoppers….the business opportunity just lets people make money faster….THAT IS IT.

The way this article and many others about Lyoness on this site is worded you would think that we pressure people into coming in with money and promise rich rewards to all that can hear.

We have separate meetings for business builders and separate meetings for merchants and separate meetings for Lyoness Shoppers. Is it completely turnkey? – not yet. if it was we would be able to get millions of people in this overnight.

That is not what these people are about. In fact several other MLM people I have approached put up a barrier and wanted to do the business their way and we never brought them on board because of that fact.

For all you know i could be making 12.59 a year, 3k per month or 150k per month. would it matter? – would it matter if i was Rik Wahlrab? not to those who THINK they know what this is.

Will I be labeled on this site as another one of “those” people who as you have written “Typically a Lyoness affiliate reads the review and then proceeds to leave a long-winded comment “educating” myself and readers on the merits of the Lyoness merchant shopping network.”

Maybe.

the documentation about the IDS shows very clearly the high the low and the average. – the people in Level 1,2,3,4,5,6,7, and 8 for the most part are business builders but they COULD be shoppers as well who just introduced others who went after this and or merchants who are spending a lot in the shopping network.

We can go through all the different types of people but i think that would be worthless. the REAL issue should be why people on this site seem to think that a company should give away free money.

In any business if you don’t work why should i pay you. – i hear people on the article bitch and moan about people not getting paid or disparity between groups (premiums and shoppers) – those are TWO separate things. –

In fact the whole point to the comp plan is to entice people to actually and actively “work” the system…Introduce people to Lyoness and they will pay you…Immediately? no and they never say that and anyone that has been told they will be rich overnight has not been told the correct way. In fact i have never heard of anyone here in the USA being told that.

This statement – “You’ll find just a tiny fraction of the 10,000 investors dwarfing the money paid out to the 80,000 non-investors. Nobody who’s made any significant money in Lyoness has done so via shopping, it’s all AU investment.”

The whole point is that if you work it Lyoness will pay you if you don’t they wont – where does it say that you just come in and make money? – why would you assume or infer that this is the case…anywhere?

Let me ask ALL of your here a question….what would be the perfect MLM, direct business scenario…or ANY business for that matter?…come in and I will give you free money? – just BREATHE and money will come to you?

If the comp plan is too hard to understand and “tricky” it MUST be a ponzi or pyramid or a scam. Again I KNOW for a fact that several if not a majority of MLM’s are. – 2000 start up every year in the USA and 1% survive after the 3rd year. Where are the reviews on the PERFECT scheme?

Your quote

The money for gift card down payments goes to opening new emerging markets. – Mexico, China, Japan for example.. how do we ENTER those markets?

Hey there we have a great marketing opportunity for you as a large merchant….can you give us 3, 4, 5% discount?…Oh well how many people do you have in our contry? Oh….none……BUT we have 2 million dollars that we want to spend on yoru gift cards.!…..Oh, then right this way mr. lyoness…by all means lets talk.

Is it that simple – obvioiusly not but that is the way we enter emerging markets with BIG named stores everyone is shopping at.

Can i lose my money i put forth in gift card down paymetns? – no but nobody to my knowledge has ever asked for that back. – Let me put it another way.

3k just as others have said is nothing for starting any kind of business and realistily if you are not making that money back in Lyoness within the first 6 months then YOU are the problem not Lyoness or the system.

That person would literally have to have no support and be saying the wrong things and not doing ANYTHING. and that is AFTER that person committed and took the time to move forward AS a business, As with anyting if you treat it like a hobby it will pay like one.

Your comment

If you really understood the comp plan the AU is only a small part of how we get paid – Lyoness is actually LETTING us at this moment put these partial down payments (yes i know it sounds like an investment and to a certain extent you are investing in a faster way of making money) into the system.

Hubert did NOT have to do this. – he could have just left it as straight shopping and this would have been more than enough….but the Gift Card Down Payments help EVERYONE especially the merchants since part of the monies made with those particular units are paid out in Lyoness Credit which is REAL money to the merchants.

Merchant A gives a 10% total member benefit…he/she pays Lyoness at the end of the month that 10%. if members have credit payments in their account that they MUST use at Lyoness merchants (which will account for maybe 3% of their TOTAL earnings in lyoness…the rest is cash) this is a HUGE win for them since they pay credit card fees on transactions…

If they are paid with Lyoness credit…no transaction fee…PLUS if the amount the Lyoness members pay them is MORE than they owe Lyoness at the end of the month…Lyoness PAYS them in a check. – somehow I did not see any of this in the review on this site.

We are still early in the game here in the USA but in Europe this particular situation is mainstream. It is NOT yet mainstream here yet…which begs the question of opportunity.

Your comment –

THere are restrictions on how much you can “put” into lyoness and they capped it at 3k so it would not be a rich man’s way of making money. If I bring 2 or 3 people in as Premium members….what money have I made? – pretty much nothing…18.00? 24.00? The whole point it shopping NOT bringing others in at premium.

The shopping is what will make this really cruise. Europeans can spend about 95% of thier Expenses inside Lyoness. – here in the USA we are probalby at 30% but that is growing tremendously.

Novemeber of 2012 is when they opened up the SME program and it is what is driving the shopping. When people shop they make units. – how fast? depends on the amount of shopping and what the merchants give in Loyalty benefits…we average it out to 5% but that is changing since many new SME’s are giving 10, 15, 20% and those are the ones reaping the biggest beenfits of the program.

BP gives 2%….my local restaurant gives 10% – how long woudl it take me to get that benefit using gas cards instaed of using my Lyoness memebrship at my local restaurant, or hair dreser or dry cleaners or chiropracture….etc.etc. – that is why the Main large copmanies are nice but they pale in comparison to the impact of the Local Merchant.

If you just showed this opportunity as a shopping network and not as a business then that is what people woudl get.

You cannot fault ANY company from trying to get as many business builders on or merchants as possible BUT the simple fact is that when the Ads come out on TV….AND THEY WILL…and Lyoness becomes mainstream and everything is completely turnkey and there are no more down payemtns and EVERYONE comes in as a shopper…..what will you people choose to rip on about Lyoness?

Not another one…

So you’ve bought into the investment scheme and are here to tell everybody how it’s not an investment and Lyoness is all about the shopping. Right, let’s get this over with then.

A genius is he? Here’s how Friedl himself described the core business of Lyoness as an MLM opportunity:

Genius? Only in that he’s managed to convince people such as yourself that shopping has anything to do with the Ponzi scheme he’s got running.

We wouldn’t discredit him, Lyoness’ own business model would.

Oh I agree. Crapping on about the shopping merchant network is a complete waste of time, but here we are – again and again everytime a new Lyoness affiliate joins the company, invests and then and tries to regurgitate the complete bullshit their upline has fed them here.

The AU money is paid to Lyoness and paid out by Lyoness. It has nothing to do with the shopping network. Nothing is bought and sold, with a cash ROI paid out only on condition of a fixed number of new investments being made with Lyoness.

Lyoness skim a bit off the top, that’s where they make (some) of their money.

Or if they invest in AUs. AAs for the lack of fees, completely irrelevant to the mechanics of the AU investment scheme.

You want to focus on completely irrelevant points? So be it, you’re on your own there son.

About as relevant to the AU investment scheme as the fact that cows like to eat grass. Oh and with whom have Lyoness registered with as an MLM in the USA? Do tell…

No they don’t.

I pay Lyoness my initial investment, and once enough new investments have been made with Lyoness, then Lyoness pay me out my >100% cash ROI.

Pop quiz: When you signed up and invested as a Premium member, did you pay Lyoness or someone else?

I sign up to Lyoness, I invest with Lyoness under the guise of purchasing AUs and either recruit new investors or wait for my upline to do it. What shopping?

It’s not funny at all, it’s completely irrelevant. If you want to read up on Lyonesss’ charity contributions hit up the spammy press release websites or affiliate cheerleader blogs.

We’re discussing the Lyoness business model here, not company-supplied talking points affiliates can use to try to divert attention away from it.

Only if they invest in AUs. There it is folks, the investor recruitment mechanic in motion.

I invest in AUs with Lyoness, I convince others to do the same and Lyoness pay me out a >100% cash ROI.

People who invest in AUs are not shoppers. Lyoness pay me a >100% cash ROI for doing nothing more than recruiting new affiliates who also invest in AUs.

And since when was “make money” different to “getting paid”?

You and I know they aren’t, so let’s not waste anymore time with fantasy scenarios. Anybody who has made any decent money in Lyoness has invested in the AU scheme and then recruited and convinced others to do the same.

It’s not free when you’re investing in AUs. Your cash ROI comes out of newly invested money, so that’s not “free” either.

Oh I agree totally, I’ve said time and time again the AU investment scheme has nothing to do with the merchant shopping network. You’re the one crapping on about how the merchant network has anything to do with investing in AUs.

The problem?

The “work” is invest money in AUs and then recruit and convince others to do the same.

Of course not. You have read the original BehindMLM Lyoness review right? All analysis is based directly on the mechanics of the compensation plan, with particular attention paid to the AU investment scheme as, firstly that’s where all the money is made and secondly it single-handedly draws the entire opportunity into disrepute.

ORLY? So merchants are not paid for their gift cards then?

You have a shopping network, the absurdity that you need to “buy your way” into a country is just that, absurd.

Nevermind the cash downpayment in AUs that pays out a cash ROI and has nothing to do with giftcards.

Right, in that you failed to recruit enough new affiliates who in turn made enough new investments so you can get paid. Blaming the affiliates is Ponzi 101.

You should have just opened with that. You understand it’s an investment (sounds like? Please, it is an investment), you understand it’s a “faster way of making money”… so why include all the other irrelevant garbage about the shopping network, charities, and merchants?

You invest in AU with Lyoness, Lyoness pay you a cash ROI once enough new AU investments have been made by other affiliates. Lyoness have been “letting” affiliates do this since they initially launched back in 2003. It’s a core component of the compensation plan.

But he did anyway, and in his own words admits it’s the whole point of Lyoness as an MLM business opportunity. Invest in AU positions and get others to do the same.

There are no restrictions, you restricted yourself buying in as a Premium member. You can invest in as many AUs as you want, outside of the predefined Premium package.

I can still invest today in AUs in European countries that Lyoness has been operating in for a decade now, so I’ll go with your full of shit.

To put it bluntly, if can’t see how investing in AU’s and receiving a >100% cash ROI after enough new investments have been made is not a Ponzi scheme – you’ve failed, miserably.

So no where do I see any mention of all the money that comes into the program from all the cash back and credits from the actual merchants. All that is discussed is the people who pay in to become a premium member.

If being a loyalty member generates anywhere from 2% to 20% cash back in the form of cash or loyalty benefits for everyone in your network who shops, I would think that would add up to quite a bit if you have 10,000 under you after a year of working at it if you chose to.

That’s because it has nothing to do with the AU investment scheme side of things. You’ll also observe the price of fish in China was not discussed in the article either.

Not nearly as much if you have 10,000 AU investors under you after a year of “working at it”. Therein lies the problem, the AU investment scheme is what really drives Lyoness as MLM business opportunity.

I was pressured into investing the $3000 investments and units by a close friends and people I trusted. At the time we did not have access to see the accounting program and how it worked. Only when you become a premium member do you get to see a live “Accounting Program”.

Once we gained access, I stopped sharing this “opportunity” because it is very Ponzi-ish because your 7 units cannot payout until you find $21,000 worth of units.

In addtion, only the people in your direct chain of upline and new people that you find to invest can place units into your accounting program to pay out the final $675 + $198 (this broken into several payout along the way to 35 units above/ 35 units below.)

With that said, I have 7 units in Accounting Program 1 that will never pay out unless I find enough people to place 70 units granted those units are balanced with 35 above and 35 below. I can have 1000+ units above, but if I only have 33 below, a unit can not payout.

The problem with this system is that in theory and ideally it CAN work. But in reality it is very, very, very difficult. In addition, once you’ve worked out the numbers like I have, then you’d have to have no conscience and be willing to get other people you know to invest another $5250 into your Accounting Program 1 just to pay your first unit.

After the 1st unit pays $675, it will take another $2625 to pay out each next unit. In order for all 7 of my units to pay out, I will have had to find $21,000 to plug into MY accounting program.

If my accounting is right, the total collective investment = $21,000 with total ROI $6411 ($4725 + $1386 in commission + 4 bonus units valued at $300).

This was sold as a system where a collective of shoppers could place $75 units behind each other’s units. But far from the truth, only people that are recruited by people you’ve recruited can benefit your units.

That means you will never get a payout unless you recruit enough people who then places $5250 worth of units. . . . Ponzi? When no one is left to join you, all the units that remain will be stuck.

But what if we shopped for these units?

Let’s break that down. When I buy $100 worth of gift cards from Walmart, Walmart gives a maximum of 2% that I can put into buying and placing units. To get $75, I will have had spent $3750.

Theoretically, all the people in my collective shopping team will need to spend $262,500 to generate the 70 units required to pay out my 1 unit – $675.

I’ll leave it here and have you decide.

The AU program doesn’t make any sense if you don’t recruit minimum 4 other investors (Premium Members), and they recruit some, and they recruit some (in an endless chain). But the average member will only be able to recruit slightly less than 1 other members.

You can POTENTIALLY get your money back if you’re asking the right types of questions to Lyoness’ support (ask questions rather than demanding something). “Right types of questions” will be about building up your own case.

You will find a list of other Lyoness articles by clicking on the Lyoness company name, right under the headline in this article. A similar list can also be found via the menu system to the right, under “Companies”.

I’m not asking you to read tens of articles or hundreds of comments, only to get a quick overview for what type of information you can find.

Eric Breiteneder, the Austrian lawyer, used plain and simple consumer logic to negotiate settlements for his clients (100% back for consumers, 75% back for business owners).

He did NOT focus on pyramid scheme issues, investments or anything like that, but simply on “This program hasn’t delivered what it promised to my clients during the marketing campaign. My clients want their money back and to cancel the deal.”

An important factor in his strategy was to bring in a third party (a court), to bypass Lyoness’ defense system.

Lyoness’ legal defense system is set up so that disputes between you and Lyoness will have to be resolved by arbitration (1 judge, no appeal, contracts will be interpreted literally as they have been written even when the terms and conditions violates other laws in reality).

That means you will need to find other solutions to the problem than a direct dispute. You will need a step by step method where you can ask some questions first and build up your own case.

I haven’t analysed the Breiteneder case in detail, but he has obviously ignored the agreement completely, and made it become a case about misleading marketing rather than a dispute about the contracts. He has obviously asked a lot of difficult questions to Lyoness.

Great points M. I don’t know how I’m going to get my money back ($3000) without getting others to through more money at it. But what is worse is that my uncle who brought me in had invested upwards of $20,000 that I know of.

Eric Breiteneder got a preliminary order from a court in Austria. “Recruiting people into a business opportunity is NOT a business activity, it’s a consumer activity”, “consumer laws can be used” (rather than the contract where the members are identified as independent business owners).

The members are NOT “business men” in reality (in their relation to Lyoness). Not even the merchants are “business men”, i.e. recruiting people into a third party income opportunity isn’t a “professional business activity” (it’s actually highly unprofessional).

Eric Breiteneder used a logic like that to bypass the contracts. I haven’t analysed the details, only the type of idea he used. But he probably documented some facts about the marketing campaign, some written material.

Bringing in a third party authority (e.g. consumer protection authority) will bypass the contracts. A consumer protection agency in Austria analysed the contracts, and found 61 points to ctiticise, and the contract as a whole to be completely impossible to understand for an average consumer = illegal in Austria.

It can be found in the article Lyoness CEO: “It’s all about positions”, in the second video there.

K Chang:

Really a cheap shot at chiropractors. They do great work and we have had the same one for over 20 years. His work with our daughter ended her need for asthma puffers. He keeps us and our children well. And no, he is not asked for financial advice.

You are normally right on with your comments, but not in regards to the chiropractors. Next time skip the cheap shots.

Michael, Moncton, New Brunswick, Canada