Family First Life Review: “Aggressive compensation” insurance?

![]() Family First Life operates in the life insurance MLM niche.

Family First Life operates in the life insurance MLM niche.

The company was founded in 2013. A corporate address in Connecticut is provided.

Heading up Family First Life is CEO and President Shawn Meaike.

Heading up Family First Life is CEO and President Shawn Meaike.

As per Meaike’s LinkedIn profile;

After I graduated with my Masters Degree I obtained a job with the state of CT as a social worker and I also obtained a real estate license to supplement my income.

For 15 years I worked two jobs to just keep my head above water.

When I was introduced to this opportunity, I was excited about one thing at first.

NAA had thousands of leads that we’re filled out and signed by clients that WANTED insurance and I got paid on average $550 for each person I helped.

In 2008 I worked part time with NAA and earned $296,000 in my first 12 months… I was FIRED up!!

I quit both my jobs and worked with NAA full time and the year after I earned $602,000.

This past year I 1099’d 1.4 million dollars.

I never dreamed about being a millionaire, I just wanted to help people and I was afraid to be broke.

Andy Albright the president and CEO of NAA personally mentored me and taught me how to follow the very simple system NAA has in place.

“NAA” is National Agents Alliance, another life insurance MLM.

While Maike’s LinkedIn profile might sound rosy, his split with NAA in 2013 was messy.

As alleged by NAA;

On December 12, 2013, Meaike notified NAA that he was terminating his employment.

NAA asserts that prior to Meaike ending his employment with NAA, Meaike formed FFL and actively recruited other agents employed by NAA to join FFL.

Later in December 2013 NAA’s parent company, Superior Performers, filed suit against Maike and several former NAA agents.

In their lawsuit, NAA alleged;

The solicitation of NAA’s agents was a violation of the Agent Agreements by each Defendant.

Upon information and belief, Meaike, (Marc) Meade, and (Bryant) Stone have also each violated the non-competition provisions in their Management Agreements.

Meade is a top Family First Life affiliate. I couldn’t find any current information on Bryant Stone.

NAA’s lawsuit against Meaike was lengthy, coming in at just under 400 filings.

The case was settled following mediation proceedings in January 2017.

In May 2014 NAA filed an additional trademark infringement lawsuit against Family First Life.

That case was dismissed relatively early on in February 2015.

Naturally it follows that Meaike’s time at NAA influenced the launch of Family First Life.

That said Meaike appears adamant in marketing presentations that he’s running the company his own way.

Read on for a full review of Family First Life’s MLM opportunity.

Family First Life’s Products

Family First Life market life insurance policies written by third-party carriers.

There is absolutely no specifics about life insurance policies anywhere on Family First Life’s website.

Instead Family First Life’s website is dedicated to marketing the company’s income opportunity.

Family First Life’s Compensation Plan

Family First Life don’t provide a copy of their compensation plan on their website.

I tried to source this information elsewhere but came up blank.

What Family First Life do provide is a vague breakdown of their compensation plan.

Cross-referencing this with official marketing videos, here’s what I was able to ascertain.

First Year Policy Commissions

Family First Life affiliates earn a first-year commission on each policy they sell.

The company’s website details a 90% commission paid on first-year monthly premium fees.

Further research reveals Family First Life’s first year policy commission rate ranges from 80% to 140%.

Specific first year policy commission rates are determined by monthly personal policy volume or total downline monthly policy volume.

Note that in both instances a commission rate is qualified for by satisfying required policy volume for two consecutive months.

Personal volume first year policy commission rates range from 80% to 110%.

- starting first year policy commission rate – 80%

- generate $5000 a month in policies for two consecutive months and earn 85%

- generate $10,000 a month in policies for two consecutive months and earn 90%

- generate $15,000 a month in policies for two consecutive months and earn 95%

- generate $20,000 a month in policies for two consecutive months and earn 100%

- generate $30,000 a month in policies for two consecutive months and earn 105%

- generate $40,000 a month in policies for two consecutive months and earn 110%

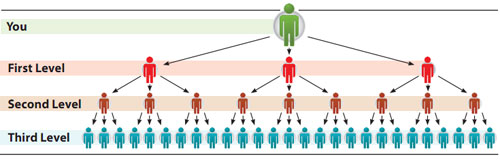

Downline volume first year policy commission rates are tracked via a unilevel compensation structure.

A unilevel compensation structure places an affiliate at the top of a unilevel team, with every personally recruited affiliate placed directly under them (level 1):

If any level 1 affiliates recruit new affiliates, they are placed on level 2 of the original affiliate’s unilevel team.

If any level 2 affiliates recruit new affiliates, they are placed on level 3 and so on and so forth down a theoretical infinite number of levels.

Downline volume (GV) is capped at up to 50% of required volume per unilevel team leg. It also includes an affiliate’s own policy volume.

- generate $15,000 GV for two consecutive months and receive a 90% first year policy commission rate

- generate $20,000 GV for two consecutive months and earn 95%

- generate $25,000 GV for two consecutive months and earn 100%

- generate $75,000 GV for two consecutive months and earn 105%

- generate $100,000 GV for two consecutive months and earn 110%

- generate $125,000 GV for two consecutive months and earn 115%

- generate $150,000 GV for two consecutive months and earn 120%

- generate $200,000 GV for two consecutive months and earn 125%

- generate $250,000 GV for two consecutive months and earn 130%

- generate $300,000 GV for two consecutive months and earn 135%

- generate $350,000 GV for two consecutive months and earn 140%

Note that once a first year policy commission rate is qualified for, it is kept regardless of future monthly policy volume production.

Family First Life calculates direct commissions based on the projected total annual fee payment.

75% of the calculated annual policy commission is paid upfront.

The remaining 25% is paid across monthly ten to twelve of the policy.

For the 100%+ commission rates, presumably there’s some “borrowing” of policy fee payments beyond the first year.

Second Year Onwards Policy Commissions

Family First Life are vague when it comes to commissions paid on policies after the first year.

Renewal Commissions are paid Annually on certain types of policies when the contract renews at the end of the year.

The average renewal commission is 5% of the Annual Premium.

Commissions are only paid on “certain” policies and no specific percentages are provided.

Residual Commissions

Family First Life are equally opaque about the MLM side of their business.

We know residual commissions are paid as overrides, in that higher ranked affiliates collect percentage differences against lower ranked affiliates in their downline, but specifics again aren’t provided.

The override commission is equal to the difference of commission levels between you and your agents.

The average override commission is 15% of the Annual Premium.

This would suggest that the 90% example cited for First Year Policy Commissions is not fixed.

Typically override style commissions are tied to rank. Such that there are ranks within Family First Life, details aren’t provided on the company’s website.

Bonuses

In one Family First Life marketing video I cited Shawn Meaike referencing bonuses, awarded to affiliates when those under them hit 140% commission rates.

No specific information beyond that was provided.

Joining Family First Life

Family First Life affiliate membership is free.

The company emphasizes that it does not have its affiliates sign any contracts.

Conclusion

I get the sense from the Family First Life marketing videos I watched, that Shawn Meaike is a pretty straight-forward guy.

I don’t know him from a bar of soap but he came across as pretty candid about the business. Which begs the question why is there no detailed compensation material provided?

I found this strange seeing as Meaike was otherwise upfront about various figures pertaining to the business.

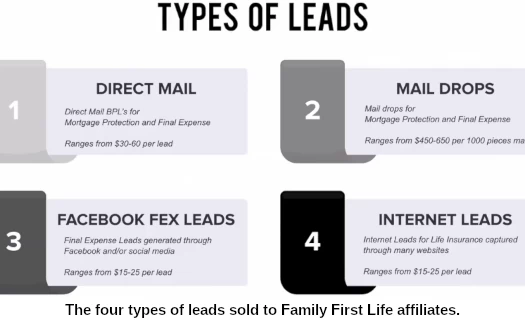

Family First Life’s basic business model is sign up, purchase leads and sell life insurance policies.

The leads are purportedly provided through third-parties, with Meaike claiming Family First Life doesn’t get involved.

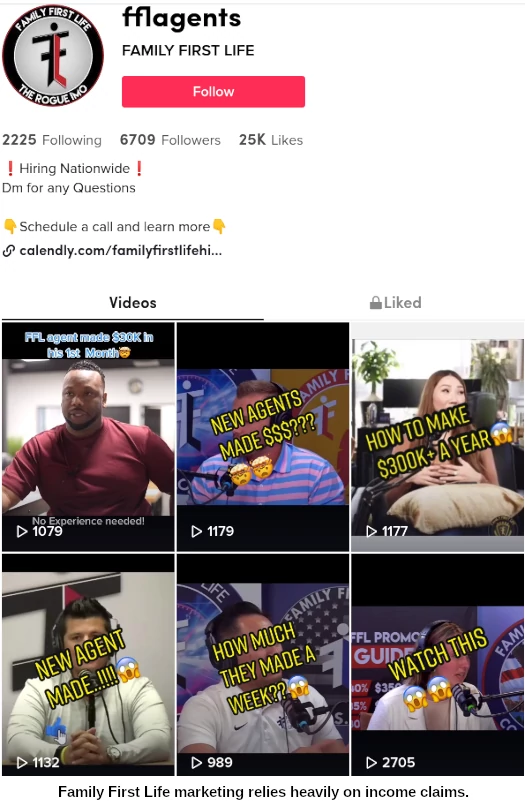

Apparently this is a successful marketing strategy, with Meaike boasting Family First Life affiliates have access to “hundreds of thousands of leads”.

[9:02] We get millions (of leads). I mean we can produce leads like we couldn’t hire… if a hundred thousand people watched this and everybody joined and everybody sold, we’d have enough leads.

Meaike claims these are warm leads, i.e. the “leads came to us”.

Attached to this is what the company refers to as “aggressive compensation”, topping out at 140% per policy. Family First Life claims the “average paycheck per policy is $675”, which is “well above the industry average”.

What Family First Life comes down as an MLM opportunity is whether you can capitalize on the leads provided. Or get your downline to.

Indeed personal policy sales will only get you so far. If you want to max out Family First Life’s compensation plan you’re going to have to build a downline.

This is an MLM company after all so that’s not a negative.

Theoretically Family First Life can wade into pyramid scheme territory, if the majority of policy holders are affiliates.

Given the company pushes the “buy leads, sell to leads” marketing so heavily, I don’t think that’s the case. Hell given the required policy volume it’d be a hefty challenge even if you tried.

What I can’t attest to or even gauge is the quality of Family First Life’s leads (provided through undisclosed third-parties).

And this leads us into a trap you should very much be aware of. With Meaike talking up provided leads up the wazoo, this sets the stage for “it’s not us, it’s you”.

While that might very well be true in some cases (selling life insurance isn’t going to be for everyone), it also can trap people in an endless cycle of buying leads that don’t go anywhere (for whatever reason).

Signing up for Family First Life might not cost anything but buying leads does. And that’s a financial trap to watch out for.

Based on what you’re comfortable spending (whatever you do don’t go into debt buying leads), set specific lead purchase goals for a few months and stick to them.

See where you’re at then and evaluate. If the leads aren’t converting, don’t get bogged down on assigning blame. It could be you, it could be the leads. It could be both.

Cut your losses and move on.

Falling into the “if I just buy a few more leads I might make a sale” trap, is the biggest financial risk with respect to Family First Life as an MLM opportunity.

Needless to say if you’re not comfortable with buying leads and following up on them, Family First Life isn’t for you. That’s their business model, there’s no changing it.

Something else to keep in mind is a 140% commission doesn’t come out of nowhere. You’re banking on your clients to keep their policies for over a year.

If that doesn’t happen, you’re on the hook for a clawback (remember, that 75% commission is paid out upfront).

Personally I’d like to see some transparency with respect to Family First Life’s compensation plan on their website. I get insurance is complicated but even some basics would go a long away.

To illustrate how this leads to confusion, the compensation example provided on Family First Life’s website details a 90% commission.

In a September 2020 Family First Life marketing video, Meaike positively rubbished this amount.

[0:31] I didn’t want anybody to be at forty, fifty, sixty, seventy, eighty percent compensation, ninety percent compensation.

I don’t care where you go but if you’re at that compensation you should quit.

Maybe that’s not the message you want to be putting out there, when 90% is the only commission example your company website provides.

One thing Family First Life do extremely well is maintenance of their YouTube channel. It’s full of content and actual training.

At the very least have a run through it before committing to anything. It should give you a sense of what the company culture is about.

I certainly think there’s a missed opportunity to integrate a lot of what’s hidden away there on Family First Life’s website.

Finally one last thing to watch out for is an affiliate looking to recruit you, hoping you and others recruited will do all the work.

There’s no minimum personal policy volume requirements across Family First Life’s upper ranks.

Make sure whoever you sign up under is actually generating personal policy volume each month, or you could be joining a dead end.

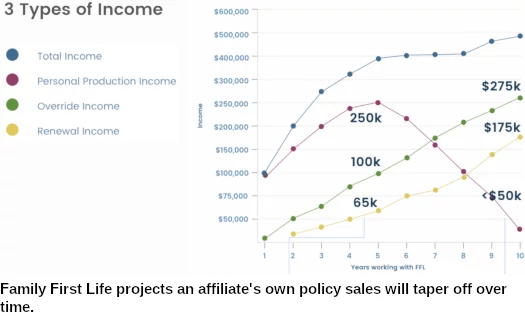

For reference, Shawn Meaike claims Family First Life’s average personal monthly policy volume is $9200 (September 2020).

Broadly speaking, insurance MLMs are complicated and there’s a lot to digest. Take your time.

Update 5th April 2022 – Sometime in the last week Family First Life has deleted the YouTube video in which Shawn Meaike rubbishes 90% commissions.

The cited video was linked in this article but as a result of the video’s deletion, I’ve disabled the previously accessible link.

I check in on your blog weekly as I have been in the MLM space the majority of my life… I’ve earned a lot and lost a lot due to my own experiences.

Family First Life was exactly what I was searching for after experiencing the ups and downs of MLM and still earning a multi six-figure income.

Insurance is highly regulated and offers the ability to educate and enroll someone with a suite of products that will benefit those they have left behind.

Due to the importance of insurance, the product has higher retention than the majority of consumable products. This awards the ability to earn large upfront commissions as high as 145% on the first 12 months of the policy and true residuals thereafter.

There are no points, or math equations to factor BV,CV,PV,PQV,GQV.. You earn on what the client can qualify for and agrees to pay for…

One similarity to MLM is the ability to build an agency, yet there is no policy and procedures (contract), no back office/website/training/conference/join fees, no parties, weekly meetings, auto-ship, hype! —

The agency consists of professionals who must study and pass the state tests /background checks so you’re not inclined or incentivized to just recruit whoever has a pulse.

If you want to keep your network/team/friends/family in the dark you can choose to purchase leads and only contact those who have raised their hand looking for insurance…

It takes real work, but this is the first place I’ve seen the reality of building a legitimate, predictable book of business where you truly can WIN without your integrity being questioned, you having to give up a check, rip a downline, cross recruit, be at the right place at the right time with the next miracle elixir just to maintain your social media status quo. #truth

Like Oz says, FFL is a MLM insurance IMO. As a former direct sales rep, my red flag with them was that they never tell the WHOLE truth about their constant bombardment of their deposit checks.

When you get that deposit as a 1099, about 60% will be spent on OVERHEAD, such as LEADS, travel cost, lodging, food, gas, rental cars, etc. You pay for EVERYTHING up front, even before you start.

If your deposit was $10,000/mo, YOUR paycheck to pay your bills is only about 40% or $4,000, even at their 100% commission level. But, they NEVER say that on any of their recruiting vids on social media.

Btw, that doesn’t include CHARGEBACKS.

Also, just to get started, you’ve got to make a sizable lead purchase of at least, $1,000 – “IF, you want to be successful”, they say, and continue to purchase that and more, EVERY week.

Well, what if you DON’T sell?! Because that WILL happen.

Also, you WILL have to travel out-of-state to run your leads. That means you’re always out of town and never home at dinner with your family. Plus, you’re talking a MINIMUM of 80/hr work week to make any decent money, which means you’re always working weekends.

Because they must recruit to build an agency (organization), they’ll never really be upfront with a newbie.

One last thing – They make it sound like EVERYBODY is making money with FFL. Well, I’ve got an ocean front property I can sell you in Arizona, too.

Oh, I forgot one minor thing – TAXES. As a 1099, you are solely responsible for paying the feds and the state, because neither the carriers nor FFL will take out the taxes from your deposits.

Genuinely surprised to see a website providing well researched information on a sector that is quite confusing to most people.

I was contacted by an individual downline affiliate for an opportunity to be a part of FFL, and this article has provided me with the information to be truly prepared about what I may be getting into, and the correct way to approach it.

There are NO other resources such as this, and I want to thank you for your honest approach to analyzing these companies.

As someone who is not familiar in any capacity with MLMs or IMOs, I was confident that this had to be a lucrative scam.

It is based on recruiting, purchasing leads, etc, but that may just be the right fit for some people. Thank you.

It is NOT the right fit for anyone.

If you get involved in these MLM, you essentially become a part of a pyramid selling/marketing scam, which is stealing money from Peter to pay Paul (Ponzi scam).

They appeal to people’s greed and desperation, as opposed to their common sense and morality.

Its sad that people are bashing what others work hard for. When someone succeeds its autmatically assumed to be a scam.

The income videos they post are very real and the people bragging about their success deserve to brag becAuse they worked very hard for that right.

The reason they post them is NOT to brag but to teach others how to do exactly like they did so others can be successful as well.

Leads are what make agents successful. You can take the slow road by bugging friends and family or you can do what tge successful peope do and invest in your business and by leads.

They teach you what works you are not under contract and can choose to run your business as you choose. Every successful agent i have followed outside of ffl do exactly the same thing such as Cody Askins or David Duford for example.

Ffl is growing and changing many peoples lives. You can do what is Proven over and over to work or you can try to reinvent the wheel and struggle or fail and complain about what the successful are doing to succeed and bash them.

But they are doing what most arent willing to do and thats why only a small percent if agents succeed. Kudos to shawn meike and ffl.

Natalie.. how’s that class action lawsuit working out.

Also, Oz might’ve touched on this, but FFL does NOT explain how the back-end (organizational) comp exactly works.

Their top rep (Taylor) just says “and you get bonuses on your group!”. Well, that’s one helluva DUMB statement to make. Is it 1%, 5%, 50%? What is it?

The owner is making his fortune on the backend of ALL the minions that work under him and all the minions know is “we got the highest comp in the industry”, which is just the tip of the iceberg.

Every MLM owner knows his/her fortune is made through the entire organization and not the front end commissions. But, nobody questions these things, which is why MOST cannot make any money on ANY MLM platform.

The broke newbie reps are just making the owners and the the guy/girl on top of the pyramid some of the richest people in each state.

Thank you for doing so much research on this company. It has been nearly a year since I first became licensed and “signed on” as an FFL agent.

Since then, I have learned:

1. If you ask for training because you aren’t “successful” they push lead purchases. As was mentioned previously, the current narrative is you must spend $1500 per week on leads to ensure success.

2. Sean Mieke owns the lead company that sells leads through the CRM. (Conflict of interest?) These leads are re-sold multiple times (up to 7 times, to be frank), though they claim to be “exclusive”. This is proven.

3. Agents are taught to “audit” the policies that have been recently sold to the leads they call. The “audit” is (of course) free to the client.

When allowed to check the policy and pricing, the agent is trained to sell another policy that is cheaper. This cuts out the first FFL agent, giving them a chargeback, and produces a commission for the second agent.

4. Agents are encouraged to sell Americo policies. Sean Mieke has very close ties to Americo. So close that he has been able to sway the company to forbid contracting to IMOs that compete with FFL.

Americo is known to rescind policies close to the two-year contestability period, leaving clients uninsured… and often difficult to insure for various reasons.

5. FFL is very forward with encouraging the sale of Americo at the outset. This ensures that another agent will come along behind and be able to undercut the first agent.

6. The “agency owners” do not purchase the same leads as the “beginner” agents. One owner accidentally slipped up and let that cat out of the bag.

7. Oh – did I mention that Sean Mieke also owns WorkSpots? (this is the subscription office space that FFL “highly recommends” agents use for a nominal $99/mo fee)

8. Between leads on credit and chargebacks, the average agent with FFL is lucky to escape under $20,000 in debt before they wake up.

The narrative to press on is strong, and FFL agency owners are great at persuasion… especially since everyone “believes” that Sean Mieke is a “stand-up” guy.

Until he threatens you on his yacht or you dig deep into the business filings and find out all that he owns… It’s all a conspiracy to pad their pockets.

The lies are deep. Don’t be fooled. It is a scam, regardless of what you hear from the people who are “making” money.

Yes- I’ve “made” over $10,000 per week in commission. Congratulations to me – It gave me $2,000 in lead cost, $4,800 in chargebacks, $250 in gas, $4,100 in federal and self-employment taxes…

So each week I’m negative $1150 for working 80 hours per week – if I don’t have any other expenses.

Great business plan.

Legally Anonymous : Well, there ya go. TRUTH from the horses mouth that every FFL rep needs to be aware of.

This is the reward you get for doing the dirtiest job in the insurance IMO with the ‘highest comp rate’?

Just shows you what a SCAM the whole insurance industry is, for anyone thinking of selling insurance.

The NAA just put out a video training about the recycled leads.

I work with FFL and have for over a year. This’ll be my 4th year in the industry (previously worked with a company who took half my commission).

First of all, I would NEVER work with an MLM OR be a part of a scam company. I’d say people who are so quick to call it a scam or an MLM clearly have never sold insurance. (Ozedit: snip, see below)

Family First Life is absolutely an MLM company.

If you can’t even admit that much then spam-bin. God only knows what other lies you tell your recruits.