LendConnect Review: LCT points ICO lending Ponzi

![]() LendConnect provide no information on their website about who owns or runs the business.

LendConnect provide no information on their website about who owns or runs the business.

The LendConnect website domain (“lendconnect.io”) was privately registered on November 14th, 2017.

As always, if an MLM company is not openly upfront about who is running or owns it, think long and hard about joining and/or handing over any money.

LendConnect Products

LendConnect has no retailable products or services, with affiliates only able to market LendConnect affiliate membership itself.

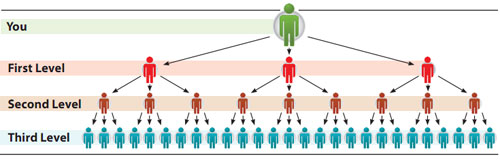

The LendConnect Compensation Plan

LendConnect affiliates acquire pre-generated LCT points from the anonymous LendConnect owners.

LCT points are sold to LendConnect affiliates for between 60 cents and $1.10 each.

Once acquired, LCT points are “lent” back to LendConnect on the promise of a monthly ROI.

- invest $100 to $1000 and receive a monthly ROI of up to 155% for 120 days

- invest $1001 to $5000 and receive a monthly ROI of up to 158.1% for 100 days

- invest $5001 to $15,000 and receive a monthly ROI of up to 161.2% for 80 days

- invest $15,001 to $100,000 and receive a monthly ROI of up to 164.3% for 60 days

LendConnect pay referral commissions via a unilevel compensation structure.

A unilevel compensation structure places an affiliate at the top of a unilevel team, with every personally recruited affiliate placed directly under them (level 1):

If any level 1 affiliates recruit new affiliates, they are placed on level 2 of the original affiliate’s unilevel team.

If any level 2 affiliates recruit new affiliates, they are placed on level 3 and so on and so forth down a theoretical infinite number of levels.

LendConnect cap payable unilevel levels at four, with referral commissions paid out as a percentage of funds invested across these four levels:

- level 1 (personally recruited affiliates) – 8%

- level 2 – 4%

- level 3 – 2%

- level 4 – 1%

Joining LendConnect

LendConnect affiliate membership is free, however free affiliates only earn referral commissions.

Full participation in the LendConnect MLM opportunity requires a minimum $100 investment in LCT points.

Conclusion

LendConnect claim to generate external ROI revenue through trading strategies”.

LendConnect claim their strategies are ‘capable of influencing prices of the coins we choose‘.

The company also claims to have a “trading bot”;

We have tested our bot and made even higher percentages than we could ever imagine.

No evidence of trading taking place or revenue generated via trading being used to pay LendConnect affiliates is provided.

Furthermore, if LendConnect’s owners actually had a trading bot generating “higher percentages than they could ever imagine”, why would they be soliciting investment from randoms over the internet?

Set the bot up and let it do its thing. Why would you want to share generated profit?

Another red flag is the LendConnect owner’s excuse for remaining anonymous.

Among other things, LendConnect’s admins claim they choose to be anonymous because they ‘hate paying taxes for reasons we’d like to keep to ourselves‘.

Putting aside emotion attached to taxation (nobody likes paying taxes), the revelation that LendConnect’s owners are willing to engage in financial fraud with respect to their own finances, likely means they’re willing to do it with your money too.

The only verifiable source of revenue entering LendConnect is newly invested funds.

Using newly invested funds to pay existing affiliates a daily ROI makes LendConnect a Ponzi scheme.

Lending ICO Ponzis like LendConnect play out as follows:

Admins (who are typically anonymous) offload worthless pre-generated points in exchange for real money. In this case it’s LCT points.

The admins then use some of this money to pay promised ROIs for as long as new affiliates sign up.

Once affiliate recruitment dries up so does the ROI reserve.

When a predetermined threshold is reached, the anonymous LendConnect admins pull a runner with what’s left.

Early LendConnect investors make a bit of money (mostly via recruitment of new investors). But same as any other Ponzi scheme, the reality of such scams is that the majority of participants eventually lose money.

One final red flag I’ll address is the sentiment that LendConnect’s owners have been active in the MLM underbelly for a few years.

We have been around in lending business since the early stages of Bitcoin and we believe now is the time to step in.

That means they probably know what they’re doing. Which means maximum money for them and screwing LendConnect affiliates out of as much money as possible when the time comes.

Just a note to say thanks for all you do to put light on the darkness in the MLM space. Much appreciated and needed.

Thanks Tom.

Surprised that you don’t mention the fact that they have a team of investors trading 40hrs/wk.

They don’t, so why would I.

The long term net return of “trading” (i.e. gambling on short term market movements) is nil, minus costs.

Even if trading takes place, trading returns will be insufficient to pay returns of up to 1,746% per annum. The only way to consistently pay investors up to 1,746% per annum is from new investors’ money, which makes it a Ponzi scheme.