IFA Review: Insurance policies and chain-recruitment

![]() IFA, which stands for Independent Field Advertising, launched all the way back in 1998 and are based out of South Africa.

IFA, which stands for Independent Field Advertising, launched all the way back in 1998 and are based out of South Africa.

IFA operates in the insurance policy MLM niche and are the network marketing division of Clientèle Life Assurance Company.

On their website, Clientèle Life claim to be

a diversified financial services group, listed on the Johannesburg Stock Exchange and is one of South Africa’s leading direct distributors of financial service products.

On the IFA website, Basil Reekie (right) is listed as Chairman of the Board of Directors. Reekie is also on Clientèle Life’s Board of Directors.

On the IFA website, Basil Reekie (right) is listed as Chairman of the Board of Directors. Reekie is also on Clientèle Life’s Board of Directors.

Reekie has a professional history in the insurance industry and joined Clientèle Life back in 2008.

Prior to his appointment as IFA’s Chairman of the Board, Reekie doesn’t appear to have any MLM experience.

Read on for a full review of the IFA MLM opportunity.

The IFA Product Line

IFA has no retailable products or services, with affiliates only able to market IFA affiliate membership itself.

Once signed up IFA affiliates can purchase various insurance policies from the company itself.

- Ultimate Dignity Plan (from R150 ZAR ($10.45 USD) a month) – “the only Funeral plan in South Africa that will pay back all your premiums on death”

- Funeral Plan (from R143 ZAR ($10 USD) a month) – “will remove the dreaded burden of funeral expenses”

- Hospital Plus Plan (from R120 ZAR ($8.36 USD) a month) – “to pay for the unforeseen expenses related to hospitalisation, supplement your medical aid if you have one or pay for everyday expenses”

- Wealth Plan (from R160 ZAR ($11.15 USD) a month) – “benefit from saving money each month”

- Foundation Plan (from R200 ZAR ($14 USD) a month) – “not only build strong foundations for your future, also save or that ultimate cash out when you need it most”

- Legal Plan (from R140 ($9.75 USD) ZAR a month) – “provide(s) you with easy access to personal legal services that are available 24 hours a day”

As per the IFA compensation plan documentation, ‘every year, on the anniversary of your policy commencement, your premium will increase‘.

IFA’s advertised policies are provided through Clientèle Life Assurance Company.

The IFA Compensation Plan

The IFA compensation plan pays IFA affiliates to recruit new affiliates who take out Clientèle Life Assurance Company insurance policies.

Commission Qualification

In order to qualify for residual (MLM) commissions, an IFA affiliate must recruit and maintain at least five premium paying affiliates.

Direct Recruitment Commissions

When an IFA affiliate recruits their first two affiliates who take out insurance policies, they are paid R200 ZAR ($14 USD).

When an IFA affiliate recruits their first ten affiliates who take out insurance policies, they are paid R1500 ZAR ($104.50 USD).

Residual Recruitment Commissions

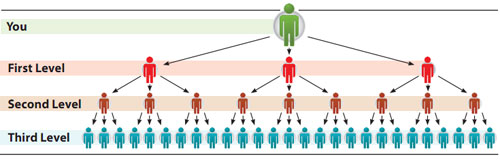

Residual recruitment commissions in IFA are paid out via a unilevel compensation structure.

A unilevel compensation structure places an affiliate at the top of a unilevel team, with every personally recruited affiliate placed directly under them (level 1):

If any level 1 affiliates recruit new affiliates, they are placed on level 2 of the original affiliate’s unilevel team.

If any level 2 affiliates recruit new affiliates, they are placed on level 3 and so on and so forth down a theoretical infinite number of levels.

IFA cap payable unilevel levels at six, with affiliates paid a percentage of monthly insurance premiums paid by affiliates in their unilevel team.

Each insurance plan has its own unilevel commission structure as follows:

Funeral Plan, Hospital Plus Plan and Foundation Plan (life component)

- level 1 (personally recruited affiliates – 12%

- levels 2 and 3 – 24%

- level 4 – 9%

- level 5 – 4.5%

- level 6 – 2.25%

Note that after one year the above percentages are reduced by 80%.

After four years IFA affiliates are no longer paid out on Funeral Plan, Hospital Plus Plan or Foundation Plan (life component) policies.

Legal Plan

- level 1 – 3%

- levels 2 and 3 – 6%

- level 4 – 2.5%

- level 5 – 1.5%

- level 6 – 1%

Wealth Plan

- level 1 – 0.75%

- levels 2 and 3 – 1.5%

- level 4 – 0.7%

- level 5 – 0.4%

- level 6 – 0.15%

Foundation Plan (savings component)

- level 1 – 0.75%

- levels 2 and 3 – 1.5%

- level 4 – 0.7%

- level 5 – 0.4%

- level 6 – 0.15%

Club Bonuses

Club Bonuses see IFA affiliates paid a guaranteed monthly income, based on how many premium paying affiliates they’ve recruited.

- Club 15 (recruit and maintain 15 affiliates) = R300 ZAR a month ($20.90 USD)

- Club 30 (recruit and maintain 30 affiliates) – R675 ZAR a month ($47 USD)

- Club 60 (recruit and maintain 60 affiliates) – R900 ZAR a month ($62.70 USD)

- Club 100 (recruit and maintain 100 affiliates) – R1300 ZAR a month ($90.55 USD)

- Club 175 (recruit and maintain 175 affiliates) – R1600 ZAR a month ($111.45 USD)

- Club 250 (recruit and maintain 250 affiliates) – R1860 ZAR a month a month ($129.56 USD)

- Club 375 (recruit and maintain 375 affiliates) – R2205 ZAR a month ($153.60 USD)

- Club 500 (recruit and maintain 500 affiliates) – R2625 ZAR a month ($182.85 USD)

- Club 750 (recruit and maintain 750 affiliates) – R3830 ZAR a month ($266.80 USD)

- Club 1000 (recruit and maintain 1000 affiliates) – R5195 ZAR a month ($361.87 USD)

- Club 1375 (recruit and maintain 1375 affiliates) – R6090 ZAR a month ($424.21 USD)

- Club 1750 (recruit and maintain 1750 affiliates) – R7035 ZAR a month ($490 USD)

- Club 2000 (recruit and maintain 2000 affiliates) – R7750 ZAR a month ($540 USD)

- Club 2500 (recruit and maintain 2500 affiliates) – R9250 ZAR a month ($644.33 USD)

- Club 3000 (recruit and maintain 5000 affiliates) – R10,100 ZAR a month ($703.54 USD)

- Club 3750 (recruit and maintain 3750 affiliates) – R11,445 ZAR a month ($797.23 USD)

IFA’s clubs purportedly go up to 20,000, however I was unable to find monthly commission rates for the upper-tier clubs.

Joining IFA

Affiliate membership with IFA is R65 ZAR a month ($4.50 USD)

Conclusion

The glaring problem with IFA’s MLM opportunity is the complete lack of retail activity taking place.

IFA affiliates sign up for insurance policies and are then paid to recruit others who do the same. And IFA are quite open about this, as per their own marketing material:

Make sure your team understands how IFA works and how they need to invite others.

Make sure that everyone in your team understands the importance of paying premiums and business fees.

As long as IFA affiliates pay their fees and recruit new affiliates who do the same, everyone gets paid.

The problem with this model is, in the absence of retail activity taking place, it’s a product-based pyramid scheme.

IFA’s insurance policies could be substituted for anything. There’s no way to determine whether affiliates have a genuine interest in their purchased insurance policy, or if they just have one or more because their IFA upline told them it was “important”.

The Clientèle Life policies seem legitimate enough on their own, but within the context of an MLM recruitment scheme are ultimately irrelevant.

As with all pyramid schemes, if recruitment in IFA dies down those at the bottom of the scheme will likely stop paying their monthly fees.

This means those above them stop getting paid, and unless they can find new affiliates to recruit, soon enough will also stop paying their monthly fees.

This effect slowly trickles up the IFA company-wide affiliate genealogy, with IFA collapsing once enough affiliates stop paying monthly fees.

To their credit IFA have been in business now for 18 years. Attrition rates and/or average affiliate earnings however are not disclosed on the IFA website. Thus the actual overall health of the business is difficult to determine.

One last point I’ll mention is the 80% commission rate drop on Funeral Plan, Hospital Plus Plan or Foundation Plan (life component) policies.

Unless I’m missing something, holders of these policies are subject to increasing fees each year while after four years, IFA affiliates cease being paid out altogether.

This is pretty shonky from an affiliate standpoint and makes it all the more difficult to build long-term residual income.

If you’re genuinely interested in Clientèle Life’s insurance polices, there’s nothing stopping you from purchasing them through Clientèle Life directly.

Every person you meet is someone you can invite to an IFA Presentation but they may not have the same goals as you. Think about the type of people you want in your team.

Before you invite someone, consider whether they would be able to pay the IFA business fee and premium.

Write down all the people you can invite to join you in IFA.

This is called a prospect list. The best prospects include friends, relatives, neighbours, social groups and people you work with.

A good introducer always follows-up with his or her team (downline).

Following-up means that you need to check on your new IFAs every week and make sure that they are doing what you are doing… inviting new prospects every day.

Unless you’re keen on being that person family and friends avoid like the plague, IFA’s current MLM model is probably best avoided altogether.

I’d like to thank whoever worked on this article. Thank you so much!

You’re welcome.

Hi Oz.

Thanks a million for this article. I am sure you have saved a lot of people’s precious time in going to affiliate meetings. I agree entirely with your views.

It is true, its a great business if you good in recruiting. You have to be patient and never relax.

Ignorance and lack of knowledge causes you to generalize the industry Network Marketing as a “Pyramid Scheme” as a whole.

Please do some real research rather than sucking out of your thumb of what you “feel” is right.

This is a review of IFA, not network marketing as a whole.

How about instead of rushing to post MLM cliches you take your thumb out of your arse and actually read the review?