AmeriPlan Review: Discount medical plans

![]() AmeriPlan launched in 1992 and are based out of Texas in the US.

AmeriPlan launched in 1992 and are based out of Texas in the US.

So the story goes;

In the early 90’s, identical twin brothers Dennis and Daniel Bloom saw the need for a value-oriented discount fee-for-service dental program, and founded AmeriPlan Corporation.

Soon Dennis and Daniel expanded their vision to include a broad array of high quality, affordable healthcare programs.

To provide greater value to the consumer, they added prescription medication, vision and chiropractic care to the program at no additional charge.

Through research, trial and error and perseverance, the brothers determined that by using the best features of the direct sales marketing model, they could provide financial opportunity to thousands of people and bring these needed healthcare programs to the public.

In addition to co-founding AmeriPlan, Dennis Bloom (left) serves as CEO and Chairman of the Board. Daniel Bloom (right) is President and COO.

In addition to co-founding AmeriPlan, Dennis Bloom (left) serves as CEO and Chairman of the Board. Daniel Bloom (right) is President and COO.

According to a 2001 article published in Network Marketing Lifestyles Magazine, the Bloom’s corporate experience began with providing marketing services for independent accountants.

As their CPA customer base grew, the Blooms wanted to be able to provide them with one-stop shopping, offering hospitalization, life insurance, mutual funds – whatever they needed.

Soon they started getting requests for a good dental program that independents could afford.

This eventually lead to the formation of a discounted fee-for-service provider access organization.

Their CPA customers loved the program … and so did their customers – The CPA’s were bringing them referrals!

Dennis and Daniel soon realized they were making more money from their little $15-per-month dental program than from everything else they were doing.

Now they knew they had found their niche.

They sold their CPA services company and in November 1992 formally incorporated AmeriPlan to market their own dental program.

On the regulatory side of things, AmeriPlan ran into problems with the Montana State Auditor.

In July, 2006

Montana State Auditor John Morrison issued a cease and desist order after charging AmeriPlan USA, its founding officers, Dennis and Daniel Bloom, and Shirl Shelley, a Montana resident, with numerous violations of both the Montana Insurance Code and the Montana Securities Act.

AmeriPlan settled the allegations a few months later for $200,000.

Under the agreement, AmeriPlan must pay an administrative fine of $200,000 and create a restitution fund for Montana customers who were duped by the company.

Montana customers of AmeriPlan can expect to receive a letter informing them that they are eligible to submit a claim to the restitution fund.

In addition, AmeriPlan is banned from marketing and selling its products in Montana for two years.

The problem, as it were, was AmeriPlan had been signing up customers in Montana despite most customers being

unable to use the discount cards because there were few, if any, providers in Montana.

Additionally, AmeriPlan (was) charged with conducting an illegal pyramid promotional scheme because it sold “broker packages” for the purpose of recruiting memberships.

Because the memberships were for discounts that did not exist, Morrison alleged there was no actual product being sold.

That, as far as I can see, is the only run-in AmeriPlan has had with regulators in twenty-four years.

Read on for a full review of the AmeriPlan MLM opportunity.

The AmeriPlan Product Line

The AmeriPlan website details three monthly subscription-based savings plans:

- AmeriPlan Dental Plus ($24.95) – “gives you immediate savings on Dental, Vision, Prescription, Hearing and Chiropractic services”

- AmeriPlan MED Plus ($24.95) – “gives you 24 Hour Access to a Doctor by phone or e-mail and immediate savings on Prescription as well as Hospital Advocacy and Ancillary Care”

- AmeriPlan Deluxe Plus ($39.95) – “AmeriPlan combo membership includes our Dental Plus discount program, MED Plus and additional non-medical discounts”

A disclaimer on the AmeriPlan website warns that ‘AmeriPlan PROGRAMS ARE NOT INSURANCE!‘

The AmeriPlan Compensation Plan

The AmeriPlan compensation plan pays affiliates to sell subscriptions to both retail customers and personally recruited affiliates.

Commission Qualification

AmeriPlan affiliates must be “active” to qualify for commissions.

An affiliate can become active by either purchasing an AmeriPlan discount subscription or selling one to a retail customer.

Direct Subscription Commissions

Direct subscription commissions are paid out on subscription purchases by retail customers.

Commissions are paid in advance, on the premise that customers will continue to pay for the subscription for at least five months.

Dental Plus or Med Plus subscription

- 1st retail customer subscription sale in a month = $19.96 (2 month advance commission)

- 2nd retail customers subscription sale in a month = $29.94 (3 month advance commission)

- 3rd retail customer subscription sale in a month = $39.92 (4 month advance commission)

- 4th retail customer subscription sale in a month = $49.90 (5 month advance commission)

Dental Plus and Med Plus subscription

- 1st retail customer subscription sale in a month = $31.96 (2 month advance commission)

- 2nd retail customers subscription sale in a month = $47.94 (3 month advance commission)

- 3rd retail customer subscription sale in a month = $63.92 (4 month advance commission)

- 4th retail customer subscription sale in a month = $79.90 (5 month advance commission)

There’s no specific mention of the Deluxe Plus membership, however I’m assuming it pays the same as the Dental Plus and Med Plus subscription rate.

Note that the advance commission rate resets each month.

Recruitment Commissions

Similar to direct commissions paid out on retail subscription purchases, AmeriPlan affiliates are paid to recruit new affiliates who sign up for a savings subscription.

The more affiliates recruited in a month, the higher the advance commission rate paid out:

Dental Plus or Med Plus subscription

- one recruited affiliate in a month = $39.92 (4 month advance commission)

- two recruited affiliates in a month = $49.90 (5 month advance commission)

- three recruited affiliates in a month = $59.88 (6 month advance commission)

- four recruited affiliates in a month = $69.86 (7 month advance commission)

- five recruited affiliates in a month = $79.84 (8 month advance commission)

- six to ten recruited affiliates in a month = $89.82 (9 month advance commission)

- eleven or more recruited affiliates in a month = $99.80 (10 month advance commission)

Dental Plus and Med Plus subscription

- one recruited affiliate in a month = $63.92 (4 month advance commission)

- two recruited affiliates in a month = $79.90 (5 month advance commission)

- three recruited affiliates in a month = $95.88 (6 month advance commission)

- four recruited affiliates in a month = $111.86 (7 month advance commission)

- five recruited affiliates in a month = $127.84 (8 month advance commission)

- six to ten recruited affiliates in a month = $143.82 (9 month advance commission)

- eleven or more recruited affiliates in a month = $159.80 (10 month advance commission)

Again there’s no specific mention of the Deluxe Plus membership, however I’m assuming it pays the same as the Dental Plus and Med Plus subscription rate.

Note that for recruited affiliates to count towards qualification, they themselves must be commission qualified.

Also note that as with the direct retail commissions, the advance commission rate resets each month.

Residual Commissions

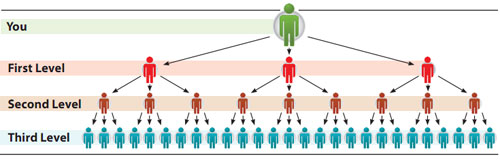

Residual commissions in AmeriPlan are paid out via a unilevel compensation structure.

A unilevel compensation structure places an affiliate at the top of a unilevel team, with every personally recruited affiliate placed directly under them (level 1):

If any level 1 affiliates recruit new affiliates, they are placed on level 2 of the original affiliate’s unilevel team.

If any level 2 affiliates recruit new affiliates, they are placed on level 3 and so on and so forth down a theoretical infinite number of levels.

Residual commissions are paid out as a percentage of subscription volume generated by generations within the unilevel team.

A generation in AmeriPlan is defined when an affiliate at the Regional Sales Director rank (RSD) is found in any individual unilevel leg.

This caps off the first generation, with the second beginning directly under them.

The second generations continues down until another RSD ranked affiliate is found in the leg.

If no RSD ranked affiliate is found, the second generation continues to the end of the leg.

Subsequent generations are defined in the same manner, with commissions payable as follows:

- Regional Sales Director (recruit and maintain one or two RSD affiliates) – 5% on volume generated by the first recruited affiliate and 10% on the second (entire downline volume)

- Senior Regional Sales Director (recruit and maintain 3 RSD affiliates) – 15% on the first generation

- Executive Sales Director (recruit and maintain 6 RSD affiliates) – 15% on the first generation and 10% on the second

- Senior Executive Sales Director (recruit and maintain 9 RSD affiliates) – 15% on the first generation, 10% on the second and 5% on the third

- National Sales Director (recruit and maintain 12 RSD affiliates) – 15% on the first generation, 10% on the second, 5% on the third, and 3% on the fourth

- National Vice President (have at least four National Sales Directors on level 1, three National Sales Directors on level 2, two National Sales Directors on level 3 and one National Sales Director on level 4) – 15% on the first generation, 10% on the second, 5% on the third, 3% on the fourth and 1% on another three generations of National Vice President ranked affiliates

Note that generations are calculated separately for each unilevel leg.

Sales Team Bonus

If an AmeriPlan affiliate’s downline sells fifty or more subscriptions in a month, a $500 bonus is paid out.

Note that only subscriptions sold by affiliates below the RSD rank count.

Centennial Club

AmeriPlan affiliates who personally generate 100 points in new subscription volume (roughly four subscriptions) a month for twelve consecutive months earn a $2500 bonus.

Vacation Trip

AmeriPlan affiliates qualify for a ‘7 days and 6 nights trip and cash bonus of $10,000‘ if they and their downline (excluding RSD and higher ranked affiliates) have sold at least 50 subscriptions each month (450 must still be active).

Cadillac Club

If an AmeriPlan affiliate earns $50,000 or more over a rolling twelve month period, they qualify for a leased Cadillac.

The vehicle will be on a four (4) year lease in your name.

You will need to maintain $4000 or more in Earned Income, each month for AmeriPlan to continue to make 100% of the payments.

The lease payments will be made directly to the lender each month by AmeriPlan.

You are responsible for any state property tax, full coverage insurance and regular maintenance.

There is no offered alternative for AmeriPlan affiliates who don’t want a Cadillac.

Joining AmeriPlan

AmeriPlan affiliate membership is $24.95 annually.

Conclusion

Personally I don’t believe “savings” is a legitimate MLM product. Reason being you’re not actually selling anything anything in particular.

Access to savings on a product or service is hardly the same as actually selling the product or service at a discount.

If AmeriPlan were to make a case for legitimacy of savings as a viable MLM product or service, they’d have to disclose the percentage of subscription holders that utilize the offered savings each year.

I couldn’t find this disclosure anywhere on the AmeriPlan website.

The good news is there is an almost as good alternative, that being retail subscription sales.

The bad news is they aren’t required, with AmeriPlan affiliates wholly able to ignore retail subscription sales in favor of recruiting affiliates on subscription sales instead.

This begins with AmeriPlan affiliates able to self-qualify for commissions.

While there is no membership purchase required, your business will grow and flourish more quickly if you are a satisfied member and have money-saving stories to share with others.

We recommend that you purchase one of our Discount Memberships and then USE it, to SAVE money then SHARE your money saving stories with others.

To be clear, I have no problem with affiliates purchasing AmeriPlan subscriptions. None at all.

The fact that these self-purchases count towards commission qualification however is a potential problem.

AmeriPlan only market discounts with third-party providers. So if you’re going to sign up as an AmeriPlan affiliate, chances are you’re going to also sign up for a subscription.

It makes absolutely no sense for an AmeriPlan affiliate to sign up and not purchase a subscription. If they themselves don’t see the value in it, how are they going to market the subscription to others.

So given this, how could AmeriPlan discourage the recruitment of affiliates who purchase a subscription at the expense of retail subscription sales?

Easy. By excluding an affiliate’s own subscription purchase as a commission qualifier.

This doesn’t stop an AmeriPlan affiliate from signing up for a subscription. Nor does it prevent them from being ‘a satisfied member (with) money-saving stories to share with others‘.

What it does stop is chain-recruitment of affiliates with a subscription, which could potentially drag AmeriPlan into pyramid scheme territory.

In addition to commission qualification criteria, I couldn’t help but notice the advance commissions paid out on affiliate subscriptions were more than double that of retail subscription advance commissions.

Specifically, AmeriPlan pay out an advance commission of up to four months on retail subscriptions. Affiliate subscriptions however are paid out ten months in advance.

Obviously without sales data from AmeriPlan I can’t confirm for sure, but this suggests a lack of retail viability with AmeriPlan’s subscriptions.

To put that into simpler terms, you’re probably looking at about a three to four month average retention rate on retail customers and double that of recruited affiliates.

Other than the attached income opportunity, why would AmeriPlan affiliates hold onto their subscriptions for double the amount of time a retail customer might?

If anything these advance payment periods should be reversed, to place an emphasis on retail subscription sales.

That of course would require an average retail subscription length of ten months or more, which evidently isn’t the case (again, I have no hard data to back this assertion up, it’s only based on the offered retail advance commission length).

Hard data you can work with as a prospective AmeriPlan affiliate will have to come from your potential upline.

What you want to know is how many retail subscriptions they currently have active, and how many of those are older than six months.

Then weigh this against how many affiliates they’ve personally recruited with a subscription.

Make sure you get active subscription data, as total numbers might be misleading (eg. 100 retail subscription sales sold over a year but only one or two are currently active).

What you’re looking for is a healthy mix of active retail and recruited affiliate subscriptions. Too much of a slant towards affiliate subscriptions suggests the subscriptions aren’t selling without the attached income opportunity.

Not enough active retail subscriptions also suggests the same.

One other thing you can ask your potential upline is raw data on how much they themselves have saved over a period of time, versus subscription fees paid.

If AmeriPlan’s subscription savings provide genuine data, getting this information from your potential upline should be easy.

If you experience push-back and/or a reluctance to provide requested information, it might be best to consider walking away.

Good luck!

I was one of the top 5 income earners in Ameriplan, but I left Ameriplan over 4 years ago.

They are having major problems. Over half of the top income earners have left Ameriplan. For those top earners still with Ameriplan, most of them have lost 50%-90% of their income due to cancellations.

Ameriplan will never release (outside of a court order or deposition) the actual number of reps (aka: IBOs) or members (aka: customers). However they have lost over half of their memberships and sales reps.

Feb 11, 2011 – Ameriplan terminated “WITHOUT CAUSE” 760 of their reps (aka: IBOs) and this clause remains in their policy and procedure manual to this day.

Many others quit the company due to this, not willing to work for a company promising lifetime residual income while also saying they can steal it from you for no other reason then they don’t want to pay you any more and to keep your income for the 2 owners.

A number of Ameriplan IBOs sued Ameriplan for the above termination without cause.

Ameriplan fired their entire “Providers Relations” department and field reps. This generated multiple law suits against them.

Ameriplan fired over 85% of their employees.

Ameriplan is millions in debt for their HQ building, which is now up for sale.